How to Invest When it Feels Like You Have No Money

melaniedj • 19 November 2018

I hear it all the time “we don’t have any money to invest, we barely have enough to pay our bills.”

Don't worry friend, I'm here to help you out! I've been there, and I want to share with you how we changed our habits in order to live a life dedicated to becoming financially free.

I think these tips will work great for those of you who want to know how to invest when it seems like there is never enough money.

First, before I talk about HOW to find money to invest, I would like touch on WHEN you should start investing.

FIRST THINGS FIRST: WHEN TO INVEST

It's Time to Invest when you have an Emergency Fund

One, you SHOULD NOT invest until you have a fully funded emergency fund (3-6 months of household expenses).

We temporarily stopped our investing this year (and will resume in January) to bulk up our emergency fund. At the end of this year, our emergency fund will be big enough to cover one year of household expenses. Before having a kid, it was big enough to cover six months worth.

I chose to do more than six months because we have high deductible health insurance plans, so in the case we have a major expense, I want to be able to cover our deductible in cash and still have a fully-funded emergency fund.

So yes, I actually follow my own advice :)

It's Time to Invest when you are out of Debt

Two, you SHOULD NOT invest until you are out of debt . Temporarily put off all investing until all your debt is paid off (except for your mortgage).

If you have a fully-funded emergency fund and you are out of debt, it is time!

For the majority of people, if they just took a look at their spending habits, I can almost guarantee that they would be able to find the money. Remember, you don’t have to have a lot to start investing, you just have to decide to START.

Also remember… It is never to late to start.

I think when you seriously consider and evaluate your financial decisions and put them into perspective, you will find that you actually DO have money to start saving and investing.

If you find yourself in the crowd of feeling like there is never enough money at the end of the month, or if you just want to free up more money to invest, use these 9 tips to help you out!

HOW TO INVEST WHEN YOU FEEL LIKE YOU HAVE NO MONEY

1. Make a Budget

If you are living above your means, you will not be able to invest. One way to ensure you live below your means is to set restraints on your spending (a budget).

We don’t like the word restraint.

The reason we don’t like it is because we have grown up in a culture that tells us we can have whatever we want, whenever we want , and to live our best life whether we can afford it or not.

I’m not against living your best life, but your “best life” is not the same as Patty next door. You have different income levels, different goals, and different family dynamics.

Just like you have a plan for your day, week, and month you need to have a plan for your finances. That is exactly what a budget is, a plan.

A budget is the law of the land.

You DO NOT break your budget. It is a contract with yourself that leads to financial peace.

If you are not sure how to start a budget, click to read my post about how to create a budget in 7 simple steps.

Also, sign up below to get my free monthly budget printable to get you started!

I also have detailed monthly budget templates in my shop!

These templates are designed to help you get your budget going immediately, and you can re-use the templates every month!

2. Calculate How Long You Had To Work to Earn What You’re About to Spend

What is the opportunity cost of what you are purchasing? How many hours did you have to work to pay for this item/experience? Is it worth it?

I do this with ALL my purchases and I can’ tell you how many times I’ve thought hell no this isn’t worth a whole day of work.

Start doing this with every single purchase and I promise you will see a change in your spending habits. That $50 iphone case suddenly doesn’t seem like such a necessity.

3. Delete Your Card Information From Online Sites

Make yourself “work” for every purchase, it will make you think twice about what you’re buying while you’re walking to get your debit card.

You know how it is super annoying when you want to buy something online and then you have to run to your purse to grab your card?

Many of us ending up saving our card information onto our favorite online sites/stores so that we can easily breeze through the checkout process without having to waste our energy on running to our purse.

Instead, delete all your card information from your favorite online sites and stores.

This way, when you go to purchase something, you have to REALLY want it because there is a cost-benefit analysis going on between the cost of the item vs. t he strain it will cause on our body to get our butt off the couch and go get our card.

4. Learn to Love Cheap Entertainment

The NUMBER ONE way you can cut costs and save money to invest is by slicing your monthly entertainment costs.

When we first got married, we were going out to eat at least a couple times a week both because I can’t cook for crap and during tax season I don’t have time to try and get better.

The result? We were spending upwards of $500 a month on entertainment! How much are you spending on entertainment every month?

I challenge you to add up every single time you went out to eat, to an event, etc. for a one month span and see how much you spent.

I can bet that it will be more than the number you estimated in your head.

Don’t tell me “I don’t keep a budget, but I have a good idea where things are at.”

To be blunt… you have no idea how much you’re actually spending.

5. Be Careful Who You Hangout With

Remember, you BECOME who you want out with.

You know those friends that everytime they want to hang out there is a $50-$100 price tag attached?

Yeah, let them know you’re ballin on a budget.

Just stop for a minute and consider the fact that if you invest $100 per month for the next 30 years, considering the average rate of return over 30 years is around 10%, you would have contributed $36,000 to a retirement account and it would have a balance of $206,284.33.

Still feel like spending that $100 a month every time you hang out with that certain friend?

Carefully evaluate how your spending habits change depending on what group of friends you are with. We all have those couple friends who frivolously spend money like it’s going out of style.

As a result, you will almost ALWAYS spend more money when you are with them either because they pressure you or because you are trying to keep up with them in your own head.

You don’t always have to say yes to plans. It is OKAY (in fact, MORE than okay) to say no.

6. Instead of What You Want Now Ask Yourself What You Want MOST

Every time you make a purchase ask yourself, how will this affect my financial goals ?

Will the purchase hinder your ability to save? Do you have to take money out of your savings to cover the purchase? Is a credit card your only option for payment because you’re cash-strapped until payday?

You have to be willing to sacrifice right NOW for what you want MOST.

Joe and I were willing to sacrifice a lavish honeymoon, extravagant vacations, and costly weekend entertainment to get ourselves out of debt. We did this by constantly reminding ourselves what we wanted MOST, where we wanted to go, and what we needed to do to get there.

The ability to delay your gratification is a skill that you can develop that is priceless in your journey to financial freedom.

7. Don’t Let Others Dictate How You Spend

We won’t be distracted by comparison if we are captivated with purpose.

Eleanor Roosevelt said, no one can make you feel inferior without your consent .

If you are constantly trying to Keep Up With the Joneses (who are probably broke), you will spend the rest of your life struggling to pay for a lifestyle that you can’t afford.

According to a report from Credit Karma, nearly 40% of millennials have gone into debt and spent money they didn’t have just to keep up with their peers.

Millennials will put off buying a house and having kids, but you can bet we’re going to have what’s IMPORTANT right now and buy ourselves that brand new car to keep up with Pam next door who has an Escalade and $50k of student loan debt she’s sitting on.

We are literally willing to PUT OURSELVES INTO DEBT (financial slavery) to keep up with others?!

8. Make Goals & Read Them to Yourself Daily

Make both short and long term financial goals and review them daily or weekly.

We all know the impact that having written goals makes on our drive and ability to accomplish them.

Make goals (include your spouse if applicable) and make sure you put them where you can see them every single day.

When making your goals, ask questions such as…

How much do we want to have saved for retirement? What do we need to invest monthly to do so? Are there costs we can cut so that we can start investing (cable, netflix, etc)?

Then, be stubborn about your goals and flexible about your methods. Figure out what works for you and your family by trial and error.

9. Avoid Debt At All Costs

It’s hard to have money to save and invest when you’re income is tied up in monthly payments.

Imagine a life without any payments. Now, work your butt off to get there. Debt is financial slavery , and there is no way around that.

In every case except for the purchase of a house, you are going into debt to pay MORE than the purchase price for an item that is DECLINING in value quickly.

Doesn’t that sound like a stupid idea? You win- IT IS!

Before you start investing, make sure you get out of debt as quickly as you can. This is the biggest reason that most Americans can't save for retirement. However, most of them don't see this as the issue because debt has been so widely consumed and heavily marketed that it is seen as a way of life.

You know what else is a "way of life" in our world today? Retiring with no money and having to work until you die.

If you're in debt, now you can quit scratching your head wondering where all your money is going and why you can't save or invest.

GET. OUT. OF. DEBT.

⭐️Related:

- The Truth About Debt (That No One Else Will Tell You)

- How to Get Out of Debt in 5 Simple Steps

- How Student Loans Cripple You

- 10 Mistakes to Avoid to Get Out of Debt Quickly

PUTTING THIS INTO ACTION…

Seriously think about the points above and evaluate your spending habits.

Your spending habits will reflect your priorities.

If someone else were to open your checkbook, what would they see? What is your top priority?

Do you spend more money on entertainment and eating out than you do giving to your church? Are you putting away the money necessary to retire with dignity? Will you be able to leave a legacy for your kids with the spending habits you’ve developed now?

Make investing a priority, and just START! :)

Share this post!

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

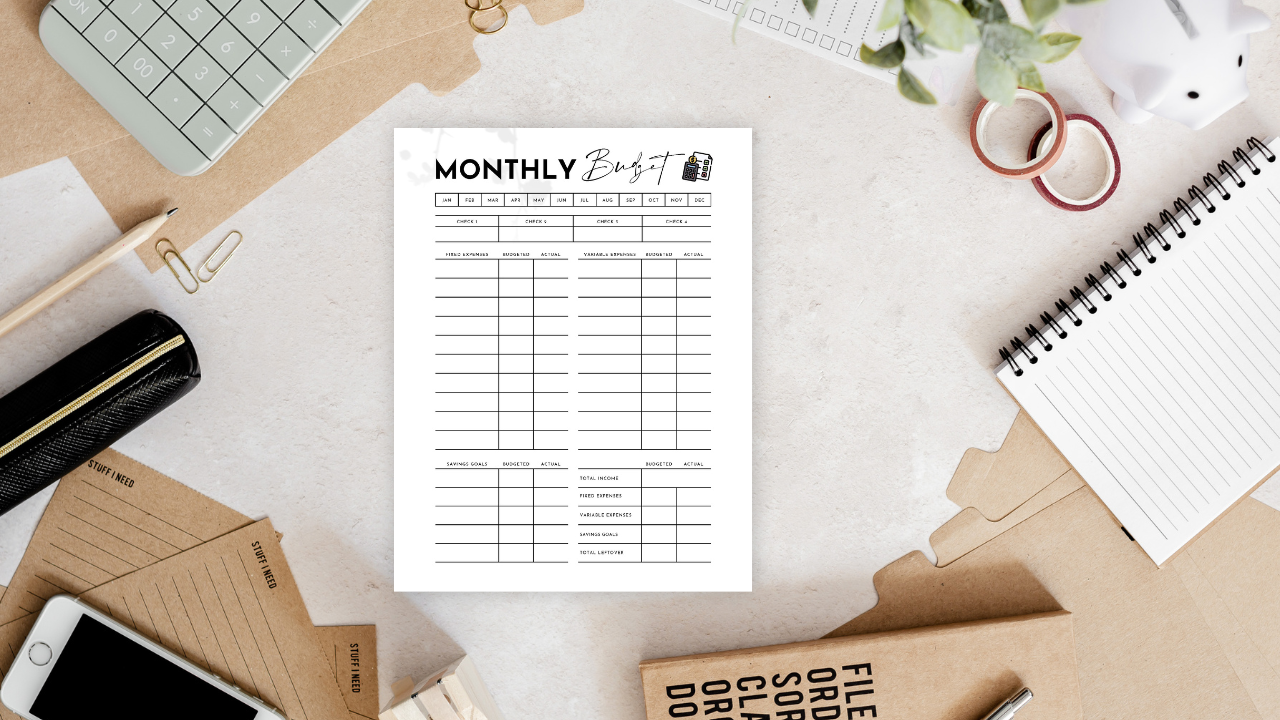

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

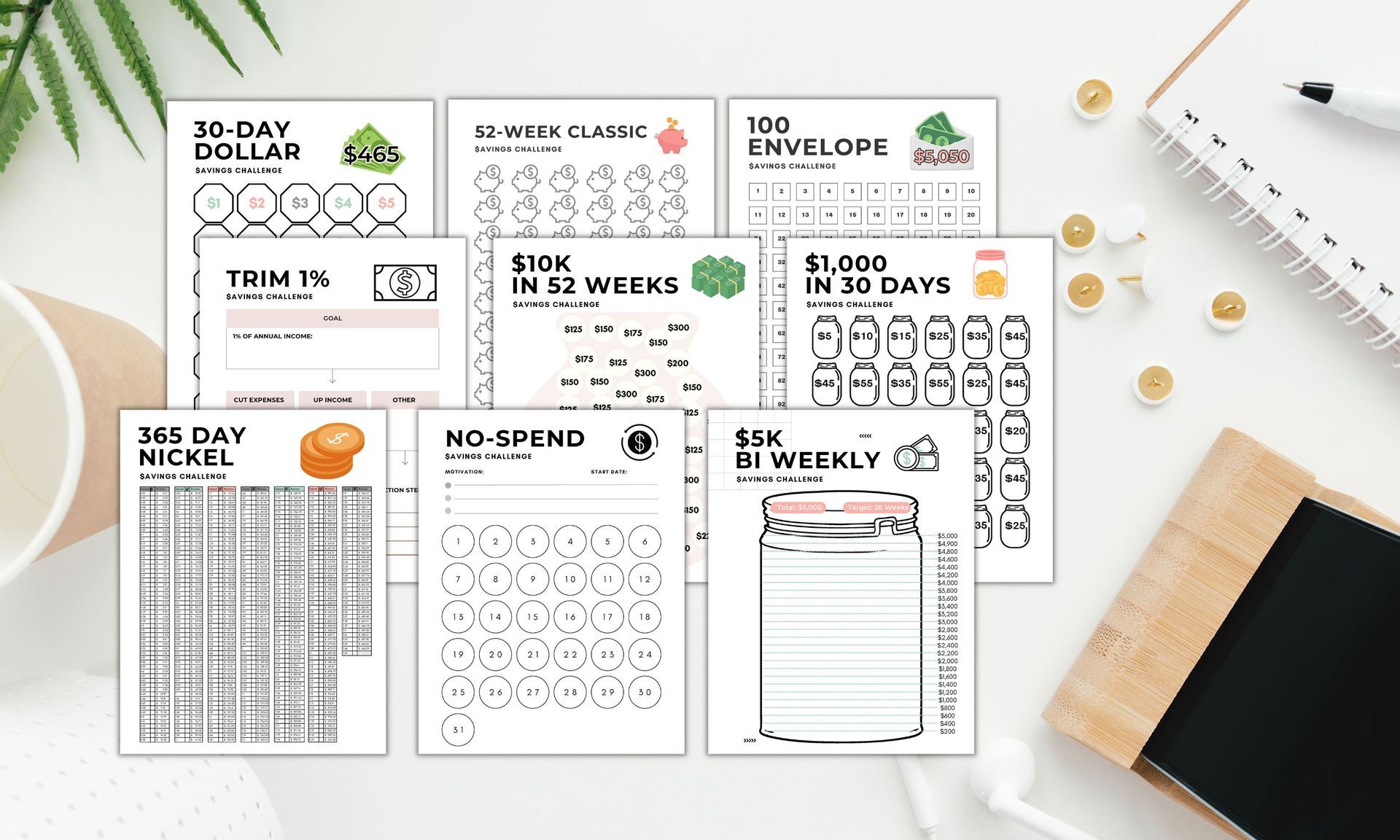

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!

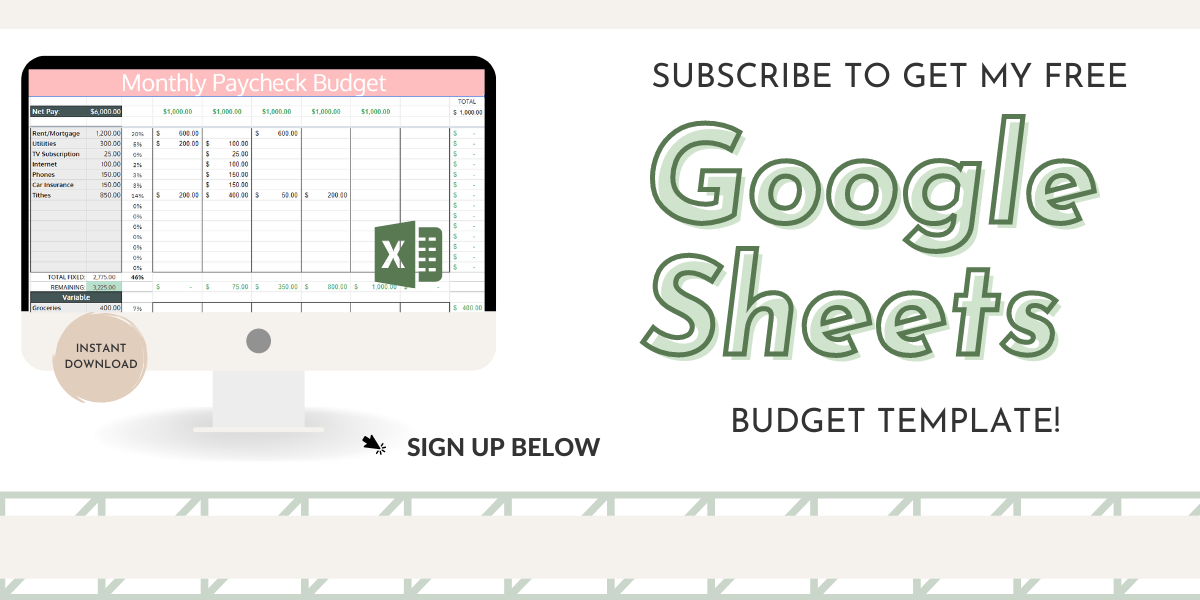

Step by step tutorial how to make a budget in excel or google sheets. Plus, get my free google sheets budget template that can be exported to excel in just a few clicks! Creating an excel budget will save you time and make budgeting a seamless process.

How much to spend on housing every month is a burning question every homebuyer asks at some point. Here's what you should consider before purchasing a home and how to determine how much you should spend on housing every month in relation to your income.