Organize Your Finances with a Free Budget Calendar Template

Melanie DeJong • 19 June 2024

A personal budget is an essential tool in your financial planning toolbox. Think of your monthly budget as your roadmap to reaching your financial goals.

While it’s important to have a budget, sticking to the budget is equally important. After all, the plan does you no good if it doesn’t work.

When I first started budgeting, life was simple. We had two incomes, no kids, and we were working on paying off my student loan debt, so our budget consisted of essentials only. Setting up and maintaining our budget didn’t require much work.

Fast forward to now, we have one income and three little kids. Because of busyness and many more expenses to keep track of, utilizing a budget calendar has been a lifesaver for our family. Clearly laying out our income, upcoming purchases, social events, and financial goals helps us see the big picture and set up our family budget for the month.

Maybe you’ve tried budgeting before and it never seems to stick, or maybe you’re a first-time budgeter looking for some guidance. Either way, it’s important to create a budget that works in tandem with your paycheck schedule, monthly bills, and other irregular and regular expenses.

One of the best ways to get a big-picture understanding of your finances and develop an effective money management systems is it to use a budget calendar.

What is a Budget Calendar?

A budget calendar is simply a visual tool to aid in the budget creation and planning process. All that is required is a blank monthly calendar and a zero-based budget template.

The monthly calendar includes all events, paychecks, monthly bills and regular expenses, debt payments, and other financial obligations.

Seeing and visualizing where money needs to go—or be assigned—will aid in the budget creation process and is a great tool to navigate the month ahead with a better understanding of our financial situation.

Why use a Budget Calendar?

Have you ever found yourself at the end of the month realizing there is more month than money left? Absent of a proper plan, this cycle continues, causing frustration and stress. Operating in this way creates chaos and disorder in our personal finances and can leave us feeling out of control – like everything happens to us—as opposed to us driving where our money is spent.

Regardless of your financial situation, being a wise steward of our incomes requires proper planning. How much money you make (or how little) is not a proper measure of financial health.

A family with a small income can be using their money more efficiently than a family with an abundance of money; the difference being one family (with the smaller income) has a plan, and the other does not.

A budget calendar is beneficial for many reasons:

- A budget calendar keeps you proactively involved in the budgeting process from start to finish. Utilize a budget calendar to keep track of your finances throughout the month, instead of totaling up spending at the end of the month and being uncertain where the budget got off track.

- Allows for even cash flow through the month by planning what bills will be paid with which paycheck.

- Reach financial goals faster as you plan for the month ahead. If you have a specific goal, use your calendar to write-in dates you can transfer money to your savings account.

- Clearly lay out and understand your financial obligations. Just like writing appointments and social events on a calendar helps you feel more in control of our schedule, a budget calendar will help you feel more in control of your finances.

Think of a budget calendar as a visual representation of cash outflow for the month ahead. Just a quick glance at your calendar will help you put together your monthly budget in no time!

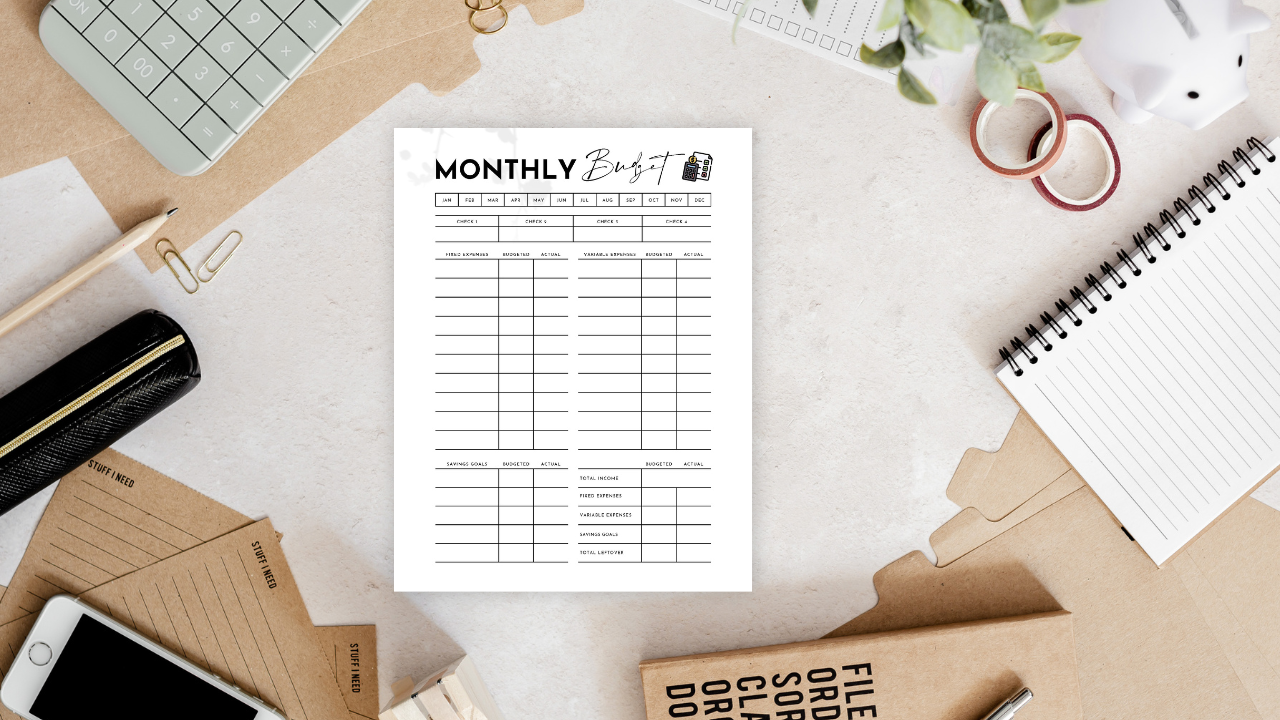

Free Monthly Calendar + Budget Calendar Templates

Before working out the mechanics of setting up your monthly budget calendar, you need a monthly budget template! I have multiple free printable budget templates to choose from:

- Microsoft excel / google sheets budget planner

- Free printable budget planner & budget binder

- PDF zero-based budget templates

These free printable monthly budget planners are free for personal use and can be printed/downloaded as many times as you’d like!

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

How to Create a Budget Calendar

1. Paychecks

The first step is to estimate your monthly income and write your paycheck(s) on your budget calendar on your pay dates (or expected pay dates). When actual paychecks come in, update your budget and budget calendar for your actual income and actual dates.

If you’re paid weekly or biweekly, the paycheck budget method is a great way to organize your budget into a weekly budget. Read more about the paycheck budget method here.

2. Bills

Write your fixed expenses on the calendar – these are your regular expenses that don’t change month to month—mortgage/rent, internet, tv subscriptions, cell phones, etc.

3. Debt

Include any

debt payments

on your budget calendar – car payments, student loan debt, credit card bills, etc.

4. Savings Goals

Many people make the mistake of having detailed financial goals, but determining they’ll figure out what’s left at the end of each month and put that towards their various goals. This doesn’t work for two reasons. One, there’s never anything left, and two, if there is, it is too tempting to use it for something else.

Determine how much you can set aside every month for various goals after setting up your zero-based budget. Then, set up an automatic transfer from your checking account to your savings and retirement accounts to discipline yourself to follow through with your goals.

Finally, be sure to track your savings goals so you can see how much progress you make over time. Download my free savings tracker to get started!

5. Variable Expenses

Your budget calendar will inform your decisions for how much to budget for variable expenses. They don’t necessarily need to be put on the calendar unless they have a due date.

Variable expenses vary month to month, such as groceries, some utility bills, recreation and activities, gifts, and fuel. Although these expenses are not fixed in nature, they should still have a maximum budget amount. For example, if upon review of your last six months of bank statements you spent between $150-$250 on fuel, you might budget $200 for fuel.

If you review your budget calendar for the month ahead and have two family outings that will require driving a longer distance than normal, you might budget $300 for that month instead of $200. Just remember, the difference ($100) will have to come from somewhere. In other words, another budget category will have to be cut $100 to keep the budget balanced. This is a true zero-dollar budget.

6. Irregular Expenses

Like variable expenses, your budget calendar will help you plan for seasonal and irregular expenses, like home maintenance, car repairs and maintenance, registration dues and fees, extracurricular activities, etc.

Once you identify recurring irregular expenses, you can set up sinking funds for them. This way, they don’t sneak up on you and threaten to blow the budget.

7. Annual Budget Calendar

If it’s your first-time budgeting, simply use a budget calendar to help you create your budget for the next month.

After you get the hang of it, start making calendars for months ahead. One of the main advantages of a budget calendar is it allows you to identify upcoming expenses and plan for them, including annual expenses like Christmas.

Customizing Your Budget Calendar

Color Code

One of my favorite ways to organize my budget calendar is to color code the calendar so that I can quickly see all our pay dates, bills, and social events. However, you can color code in whatever way you want-- whatever works for your personality.

Digital Version

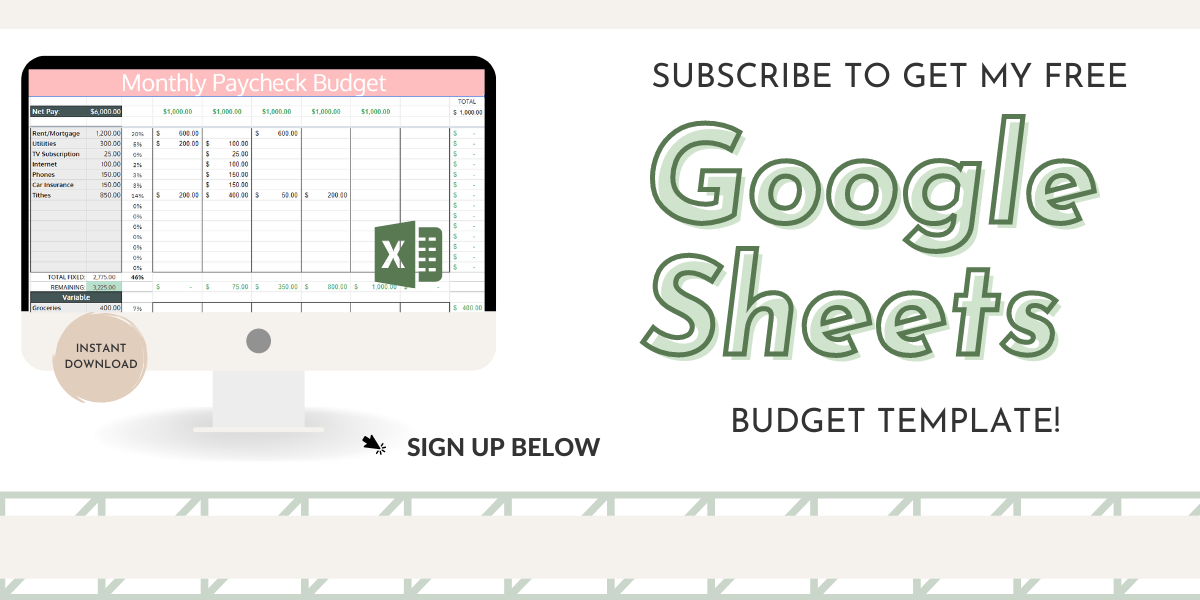

If you prefer a digital template over a written template, utilize this google sheets budget template to use alongside your free budget calendar!

Share this post!

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

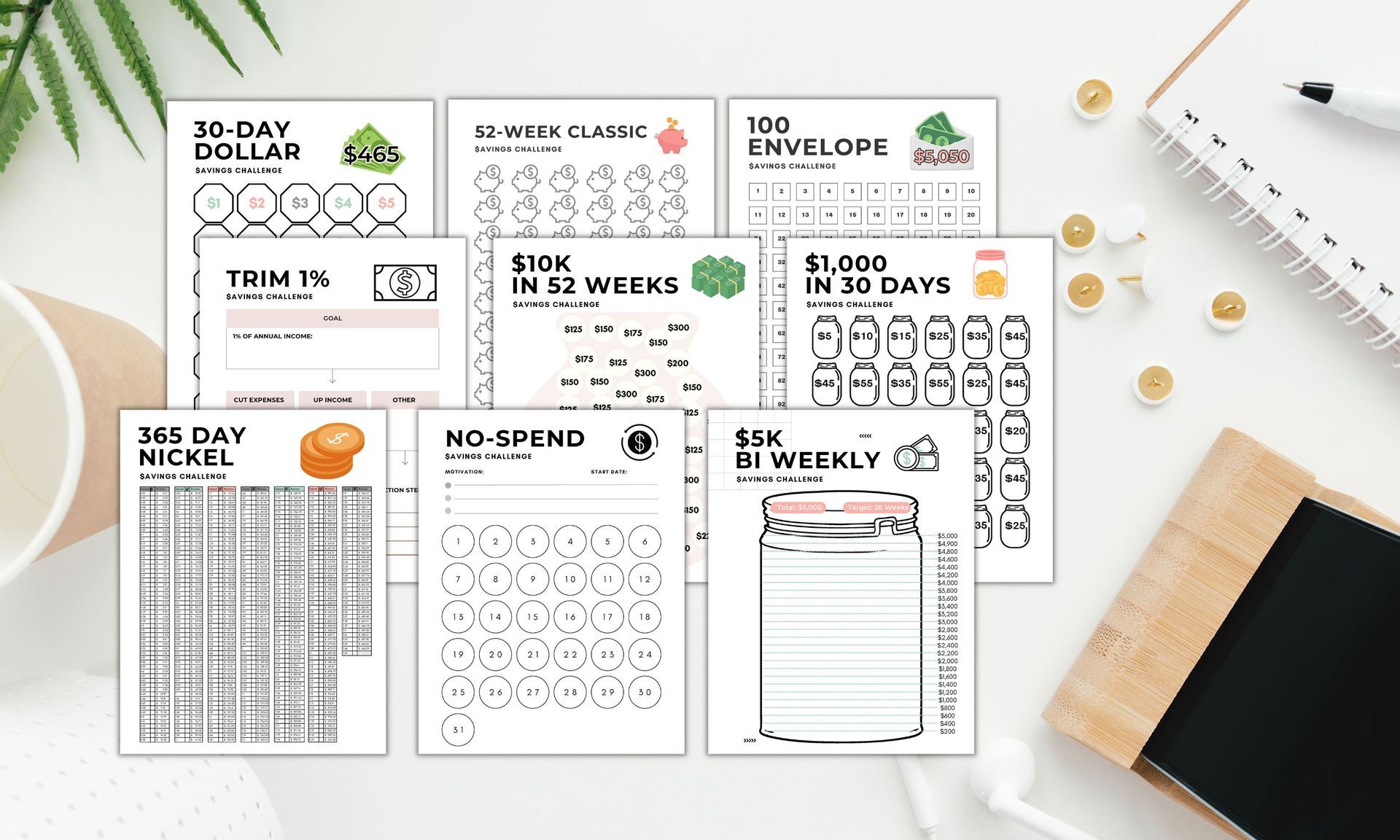

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!

Step by step tutorial how to make a budget in excel or google sheets. Plus, get my free google sheets budget template that can be exported to excel in just a few clicks! Creating an excel budget will save you time and make budgeting a seamless process.

How much to spend on housing every month is a burning question every homebuyer asks at some point. Here's what you should consider before purchasing a home and how to determine how much you should spend on housing every month in relation to your income.