13 Proven Tips That Will Help You Stick to Your Budget

melaniedj • 22 July 2019

It takes time and effort to create a budget that not only works mathematically, but also a budget that you can stick to!

A budget should be a reflection of your life.

A budget is like a mirror, it tells you the story of where your money is going and what your priorities are. It magnifies the imperfections or "holes" in your financial health.

When the imperfections are magnified, many people become frustrated and give up. They decide sticking to a budget is pointless, hard, and not worth their time.

Anything that is worthwhile isn't going to be easy, including budgeting.

Once you get the hang of budgeting and ironing out the wrinkles, it'll become easier to stick to your budget as you change your money behaviors.

Ultimately, that is the goal- to change the way you relate with money!

WHAT YOU NEED TO STICK TO YOUR BUDGET

WHY YOU NEED A BUDGET

The "why" of budgeting will look different from person to person , but a budget for everyone is about being proactive.

Here are just a few reasons we budget!

- To set a good example for our children

- It was the tool we needed to become debt-free

- Work as a team in marriage

- Save for our financial future

- Budgeting brings peace to our home and marriage

Saving for your financial future and living on a budget it not considered normal.

To be blunt, "normal" in America is broke, whether it looks the part or not. When you live on a budget and begin to say no to some things so that later you can say yes to better things, people will think you're weird!

As Dave Ramsey puts it, would you rather be broke or weird?

If you don't yet have a monthly budget template, click below or here, and you can get my free finance planner!

People who live on a budget know exactly where money is coming in and where it's going out, giving them the information they need to be successful with their money.

Saving and investing doesn't depend on how much money you make, it depends on what you're money behaviors are.

Many people who make a lot of money don't operate on a budget and scratch their head wondering why they can't find any money to save or invest.

It's time to quit lying to yourself and get real about where your money is going.

A budget is a plan, and success comes easier with a plan.

HOW MUCH TO BUDGET

To create a realistic budget that you can stick to, it helps to have some general guidelines on how much you should be spending where.

These guidelines tell you whether your spending is in relation to your income is healthy or whether it needs some work!

The recommended budget percentages (by Dave Ramsey) are:

Does your current spending allocations reflect your priorities?

Remember, I said your budget is mirror into your life , it shows where your priorities lay.

If your budget (or lack thereof) doesn't reflect your priorities, you will be frustrated and under a lot of financial stress.

Related:

13 HACKS TO HELP YOU STICK TO YOUR BUDGET

Be Realistic.

If you aren't realistic about your budget, you'll become discouraged, and eventually quit altogether.

If you tracked your spending for a couple months (without budgeting) and realized that you consistently spend $500 per month on groceries, it's not realistic to cut it to $200.

Hopefully over time you can cut that number down (depending on your family size), but be realistic.

Use a Calendar.

Have your calendar handy when you're creating your monthly budget.

Every week there seems to be some sort of celebration going on, whether it be a birthday, retirement, anniversary, baby shower.

These celebrations can be easily forgotten if you don't consult your social calendar- so have it handy while making your monthly budget!

Meal Plan.

We were able to cut our grocery bill in half thanks to meal planning. I use a meal planning service called $5 meal plan to do my meal planning for me.

As a busy wife, mom, and blogger, meal planning is one thing that had to give. For me, $5 a month to have a meal plan custom made for me every week is worth it.

Related:

Ditch the Credit Card.

Research shows over and over that people are willing to spend more with a credit card than with a debit card or cash.

Don't let the temptation of paying later overcome you and cause you to spend more than you can afford or more than what you budgeted.

Related:

Get an Accountability Partner.

If you're married, your accountability partner is your spouse. If you're single, find someone who is willing to hold you accountable for your spending.

This person should not be one of your broke best friends. This person should be someone who is financially savvy.

Keep your Goals Visible.

It's not enough to keep your budget and goals in mind, both should be written down so you have visual, daily reminders.

When we were paying off my student loans, I'd tape the "loan paid in full" notices to the fridge every time we paid off another.

This was the fuel I needed to keep going and reminding myself that paying off my loans was more important than an extravagant honeymoon.

Convert Purchases into Hours Worked.

Every time you want to purchase something, take a few seconds to convert the purchase price of the item into hours worked.

For example, let's say you're paid $20/hour. If you want to buy a $40 shirt, you had to work two hours to pay for that shirt. Is it worth it?

If nothing else, this will make you think twice and help you avoid impulsive purchases.

Pay Yourself First.

Paying yourself first refers to putting money into your saving and investing accounts first thing when you get paid before spending on other things.

We had our financial adviser set up an automatic withdrawal from our checking account every month with the amount we have designated for investing.

This has helped us tremendously because no matter what that money is coming out, which means we can't use for something else "just this time."

Related:

Set up Auto-Pay.

Automatically have your savings amounts transferred from your checking account to your savings account AND set up auto pay for your bills.

This way, the money you are saving up for a new car or summer vacation won't be accidentally spent on lobster tail and steak.

Remove Card Information from Websites.

If you're a recovering impulsive online shopper , don't allow your internet browser to save your card information.

When you browse sites like Amazon, Walmart, Etsy, etc., you make it too easy for yourself to say yes if you have your card information saved.

This is a simple way to curb bad spending habits, at least until you change your behavior.

Research Free Activities in Your Area.

Be proactive in finding frugal, fun activities for your family. If you're willing to do a little research, I'm sure you can find some free activities nearby you didn't even know existed.

One of the cheapest ways to have family fun night is to explore outdoors!

Are there any parks you can visit nearby? Are any businesses having family fun night? Is there a free day offered at the city pool?

Use Cash.

Using cash, or the cash envelope system will bring control to your spending.

If you have trouble keeping up with your online banking and reconciling your bank statements, use cash!

We use cash envelopes for quite a few categories, including groceries, personal spending, travel, date night , and our miscellaneous category.

If you subscribe to my email list below, I'll instantly send you some cute little cash envelopes to get you started... for FREE :)

Related:

Respect Your Money.

I have no doubt that you work hard for your money and it's frustrating when there never seems to be any left at the end of every month.

Learning to respect your money means learning to live within your means , in order to make your money go further and last longer.

If you budget simply so you can accumulate more stuff, you'll never master it. Of course it's not bad to reward yourself with items you've saved for, but if that's your only goal you'll never be happy or feel at peace financially.

Start respecting your money!

Share this post!

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

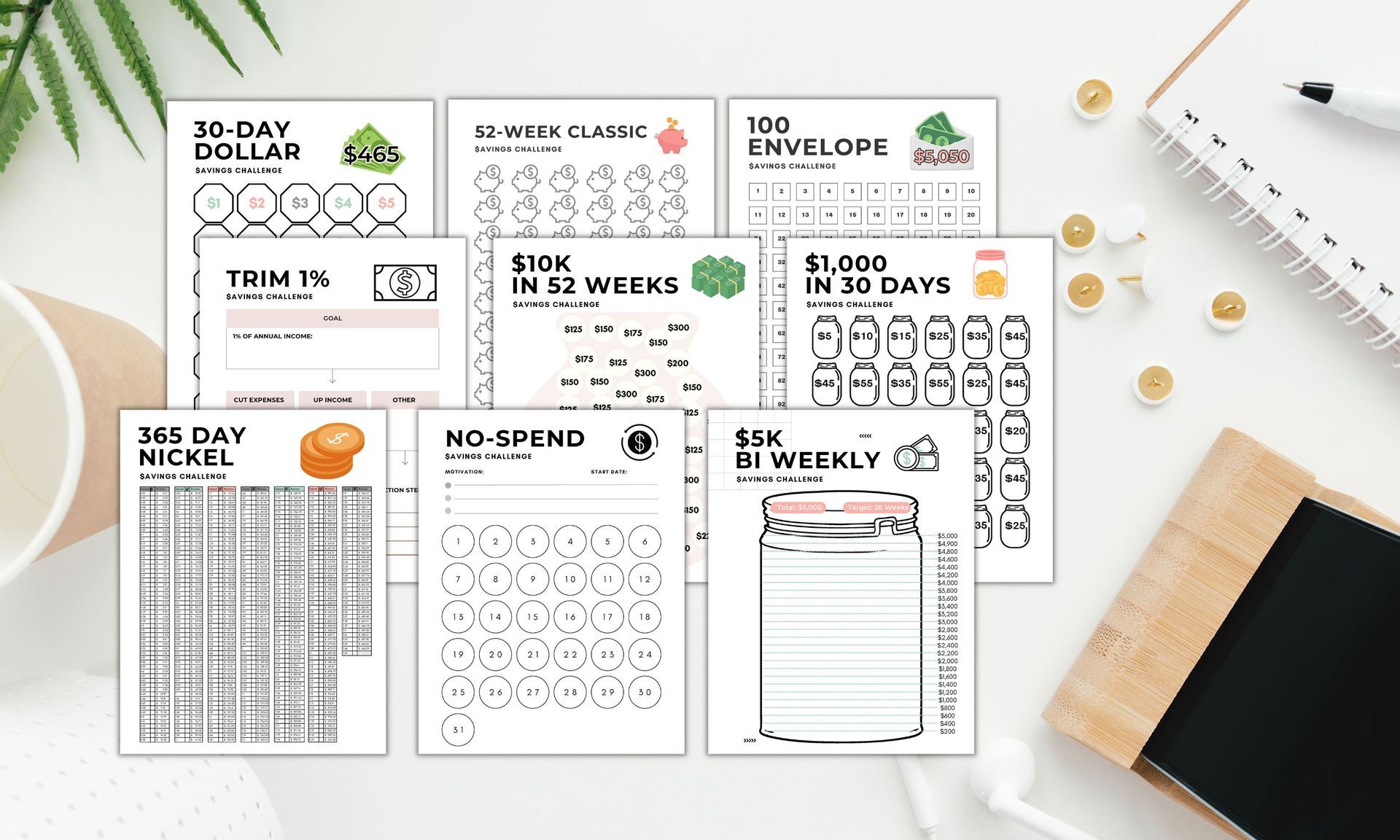

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!

Step by step tutorial how to make a budget in excel or google sheets. Plus, get my free google sheets budget template that can be exported to excel in just a few clicks! Creating an excel budget will save you time and make budgeting a seamless process.