How to Fix Your Budget When You are Over Budget

melaniedj • 14 April 2019

We've all been there. You make your perfect monthly budget to just a few days later have it blown by an unplanned bill or other expense.

Don't fret my friend, I'm going to tell you the exact process you should go through to fix your budget when you are over budget.

If you don't have a monthly budget yet, but you know that you are spending more than you make, it's time to get on a budget!

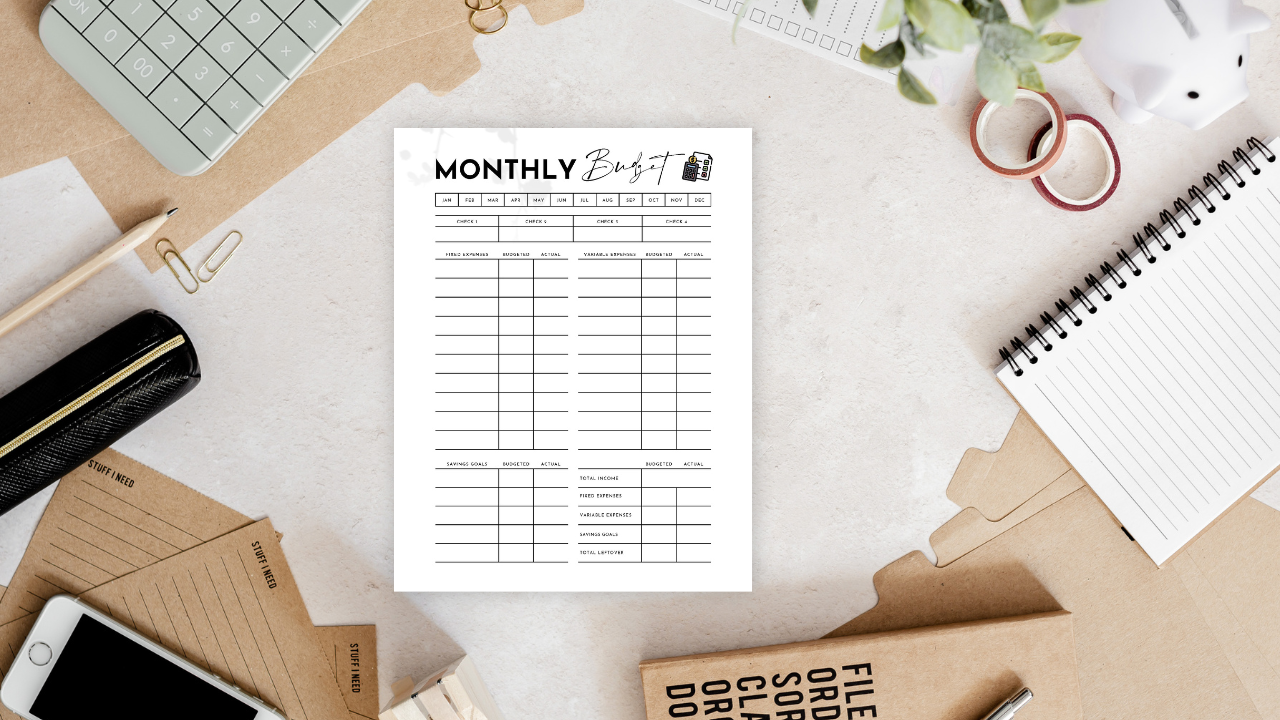

Snag my

excel budget template (pictured below) and start taking control of your money by giving every dollar a purpose.

A budget tells your money where to go every month instead of wondering where it all went.

If you subscribe below, you can get one of my FREE budget templates!

Related Content:

WHAT TO DO WHEN YOU'RE OVER BUDGET

DO NOT USE YOUR CREDIT CARD

First, you must decide that debt is not an option to cover this bill/expense.

If you have been/do use credit cards, you will be tempted to cover any budget shortages with a credit card and then cover the credit card bill with your next paycheck.

This is a huge no-no. A cardinal sin in the budget world, if you will.

Remember, personal finance is 80% behavior and 20% what you make.

When you use a credit card to cover any little shortage that comes in, you WILL turn it into a habit.

DECIDE IF THIS IS A BUDGET ITEM OR EMERGENCY FUND ITEM

Use of the emergency fund is reserved for things like loss of job, major car repairs, medical bills, etc.

Your kitchen renovation is not an emergency, no matter how many different ways you try to spin it.

If you are going to be over budget because of a something like a major unexpected car repair, evaluate using these steps:

- Can you cover this with your car repairs (or similar expense) sinking fund? If so, deplete this fund. If you don't know what a sinking fund is, click here to learn (these are a MUST).

- If you can only partially cover the expense with your sinking fund, use your emergency fund to cover the rest. First deplete your sinking fund, and if you are still short, use your emergency fund.

- Build up your emergency fund back to original balance, pausing paying off debt if applicable. If you do you have to use your emergency fund, pause paying off debt (if applicable) and build your emergency fund back up asap.

Remember, only use the emergency fund for legit emergencies.

If you are over budget because you ate out more than you allowed for in your budget, do NOT use your emergency fund, and instead continue with the steps below.

RETURN IF YOU CAN

If the reason you are over budget is because of an impulse purchase you made, return the item.

Sorry, you and Gucci are going to have to break up and you and the budget are going to have to get married. This is an arranged marriage. Some day you'll thank me ;)

When I first started budgeting, if I was feeling rebellious or emotional (these seem to be a recurrence in my life), I would go blow my budget on something I felt I deserved.

Then I'd humbly drag my sorry butt back to the store and return my purchases.

You MUST learn the discipline of returning items.

GET YOUR BUDGET UP TO DATE

If you are unable to return your purchase and/or the purchase does not qualify for use of the emergency fund, you will need to adjust your budget.

First, your budget needs to be up to date.

Don't start assessing categories you can pull from if you haven't updated your budget/spending in a few days.

Update all budget categories so that you have a true picture of where everything is at.

SIMPLE FORMULA

I use a simple formula to assess whether my budget is truly up to date:

SUM OF REMAINING BUDGET CATEGORIES - CASH ENVELOPE MONEY - SAVINGS ACCOUNT BUDGET CATEGORIES = BANK ACCOUNT BALANCE.

Su m of remaining (adjusted) budget categories - this is the adjust balance of all your budget categories. For example, I budget $300/month for groceries, which breaks down into $150 per pay period for me (I'm paid twice a month). If I started the pay period with $150 budgeted, and I spent $50, my adjusted budget balance is $100.

Cash envelope money - When you total up ALL your budget categories (including sinking funds), back out any cash envelope categories. We do this because this is money that is not actually in your bank account.

Savings account categories - If you transfer money to your savings (emergency fund money, sinking fund money, etc), you need to back these amounts out as well.

If your checking account balance and balance after applying the formula do not match, you know that you either added wrong or forgot about a purchase (or two).

FIND A CATEGORY TO PULL FROM

The most common way to alter a non-major over budget expense is to pull the money from another budget category.

What categories can you trim down for the month?

I typically trim off of our grocery budget, miscellaneous budget, or eating out budget, as I find those are my most "adjustable."

Since we budget by paycheck , I break our monthly budget down into mini-budgets every time we are paid.

For instance, our grocery budget comes out of my paycheck, and I'm paid every two weeks. We budget $150 per paycheck for groceries for a total of $300 per month.

If after the first two weeks of the month we spent $175 on groceries, then I just try to spend $125 or less the next two weeks to make up the difference.

But if i'm not able to, then I borrow from another budget category!

ADJUST YOUR BUDGET

After you decide what category to pull from, you should adjust your budget for the rest of the month to account for the changes.

If the month (or pay period) isn't over and you've overspent $30 on one category already, pull from the other category and then update your budget.

This is really simple to do, especially if you budget by paycheck.

Put your new budget on your fridge or in your budget binder so that you remember your new budgeted amounts!

DON'T LET IT BECOME A HABIT

Just because there is a "fix" to overspending, don't let it become a habit. The point of a budget is to get your spending under control.

We ALL have budget bloopers and they are inevitable!

If you are over budget, don't panic.

Follow the steps above and get your budget back on track the next month!

Share this post!

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!

Step by step tutorial how to make a budget in excel or google sheets. Plus, get my free google sheets budget template that can be exported to excel in just a few clicks! Creating an excel budget will save you time and make budgeting a seamless process.