Create a Budget You Can Stick To (5 Best Hacks)!

melaniedj • 1 February 2020

Maybe you've tried the whole budgeting thing, and you were even pretty dedicated, but you found yourself unable to create a budget you stick to.

No matter what you try, nothing seems to work and you're about sick of all this budgeting talk.

There always seems to be more bills than money, and if there is anything left over, it's nothing to write home about.

Today I want to share why your budget isn't working, and how you can fix it!

Budgeting hacks/tips:

5 WAYS TO CREATE A BUDGET YOU CAN STICK TO

1. FACE YOUR FEARS

This first tip is very simple. You need to face your fear of finding out where your finances are really at and stop making excuses.

I'm not a money person. It sounds complicated. I'll figure it out later when I'm older. I don't have time, I'm too busy at work.

You're literally telling me that you're so busy making money that you don't have time to manage the money you're working so hard to earn?

Everyone is busy. If you don't make time for your money, you'll just be a hampster on a wheel constantly trying to earn more money in hopes of keeping up with your spending and lifestyle increases.

In order to create a budget you can stick to, you need to face your fears.

2. TREAT IT LIKE A BUDGET NOT A FORECAST

One of the biggest mistakes people make when budgeting is setting up their budget and treating it like a forecast.

Budgeting requires being proactive in your finances, not passive. You don't set your budget and then turn on autopilot mode. If you do, you'll likely end up frustrated at the end of the month.

At this point, you realize you've overspent on groceries, you didn't save as much as you thought you could, and things didn't necessarily go as planned.

You painted a picture of how you wanted the month to go, it didn't go that way, and you feel immediate failure once you realize real life didn't align with your predictions.

At this point, many people give up and think what's the point anyway?

The problem is that although you might always have money in your bank account without a budget, you likely aren't prioritizing and making your money work for you.

You're simply getting by , which is what causes money stress in the first place, and thus making you consider budgeting.

CHANGING HOW YOU THINK ABOUT THE BUDGET

Changing how you think about budgeting requires changing how you think about your money- as a finite resource.

What many people don't realize is that the feeling of scarcity isn't necessarily a bad thing.

In fact, I think the opposite feeling is more harmful and detrimental to your finances- the feeling of always having enough when all you're actually doing is scraping by and living paycheck to paycheck.

TAKE THIS EXAMPLE:

Let's take a quick example.

You have $800 in your checking account today left until payday.

Your $200 electric bill, $80 phone bill and $100 car insurance bill are due before you get paid again. You also now you'll need groceries before payday, you estimate $120 worth. Even though you don't have a budget, you know that in your head.

You think to yourself, wow, we're in pretty good shape! That leaves you with $300 left until payday! You're delighted knowing that you can either use that $300 towards your goal of paying down debt or putting it into your savings for a down payment on a home. Life's good.

Except the next day you realize you're almost out of diapers for the baby, those will cost $40.

Then you look at the calendar and realize your extended family from out of town is visiting and you're all supposed to go out to a fancy steak restaurant tomorrow.

Well shoot, I guess that $300 towards your goals will have to wait until next month.

Sound familiar?

THE SOLUTION

The feeling of scarcity will either drive you to quit or drive you to make better decisions with your money.

If you want to make better decisions, give every dollar a function before the month begins based on your goals. Then, be proactive and ADJUST your budget as money actually comes in and expenses actually go out.

So how does this work with my previous example?

It's likely that when you got your prior paycheck, you immediately started spending some it (without sticking to any real budget).

You went out to dinner with friends, stocked up on groceries, and bought your spouse a birthday gift.

No feelings of scarcity, because it was payday!

However, if you had known that your savings goals wouldn't happen this month you might have planned your meals and grocery shopping more carefully. You might have invited your friends over instead of going out.

If you had made a budget before the month began based on your priorities, things might look (and feel) differently!

3. MAKE IT REALISTIC

If you're constantly adjusting your budget for overspending in certain areas, you're probably not being honest with yourself when setting your budget in the first place.

My grocery budget for our family of three is $300 per month, but if you have a family of 5 that probably isn't realistic.

Just like unrealistic diet cuts, unrealistic budget cuts don't work.

Base your budget on reality, but as a word of caution, don't use the reality of your poor spending habits to justify budgeting more than you should for certain categories.

For instance, if you're single and you look back at your bank statements and realize you've been spending $600 per month on groceries and dining out and haven't saved any money, don't set your grocery budget at $600 when you first make your budget.

That's confusing reality with stupidity.

The same goes for paying off debt. If you have a goal to pay off your student loans ASAP and you and your spouse have been spending $500 per month going out, don't set that budget at $500.

Rather, challenge yourself to set it at $150 (which is reasonable) and change your stupid money behaviors instead.

4. THINK OF IT AS A CONTRACT BUT BE FLEXIBLE

Yes, this tip sounds like a huge contradiction- how can you think of the budget like a contract but also be flexible ??

The goal of budgeting is to make what's actually happening in your finances and your priorities align by creating a plan you can stick to.

So your budget should be thought of like a contract between you, your spouse, and your money.

This way, when you are tempted to have frequent dinners out instead of taking time to meal plan so you can stick to your grocery budget- you are reminded of your contract.

However, there are times that require flexibility. Because life is unexpected!

5. ADAPT & CHANGE

When I have to adjust our budget for changes in our life, it's nearly impossible for me to have a slight feeling of failure, and that's not how it should be.

You can and you should shift your budget around for different stages of life and as your priorities change.

When you have long-term goals, it's normal to have to make adjustments as you go. This doesn't mean you've failed, it means you are living and breathing.

HOW TO ADJUST WHEN OVER OR UNDER BUDGET

On a monthly basis, you'll likely end up either over budget or under budget in certain areas. That's normal- as long as these amounts aren't consistently fluctuating by $50 or more.

Read closely, because this is a key budget concept that many don't quite get.

KEY CONCEPT EXAMPLE 1: ADJUST AS THE MONTH GOES

If you predicted $1,000 of cash per week coming in to your bank account based on your salary and halfway through the month you've only brought in $600, you need to bring out the budget and adjust it.

Adjust your discretionary expenses so that your budget balances again- i.e. what is coming in is exactly what is being budgeted.

If you set up your budget correctly for that month, you would have assigned every single dollar of the predicted $4,000 to a budget category.

As a result, if you don't adjust the budget, you'll have budgeted $4,000 for the month when you only brought in $3,600.

You'll find yourself over budget and frustrated if you don't adjust.

Thus, you'll never feel like you are able to create a budget you can stick to.

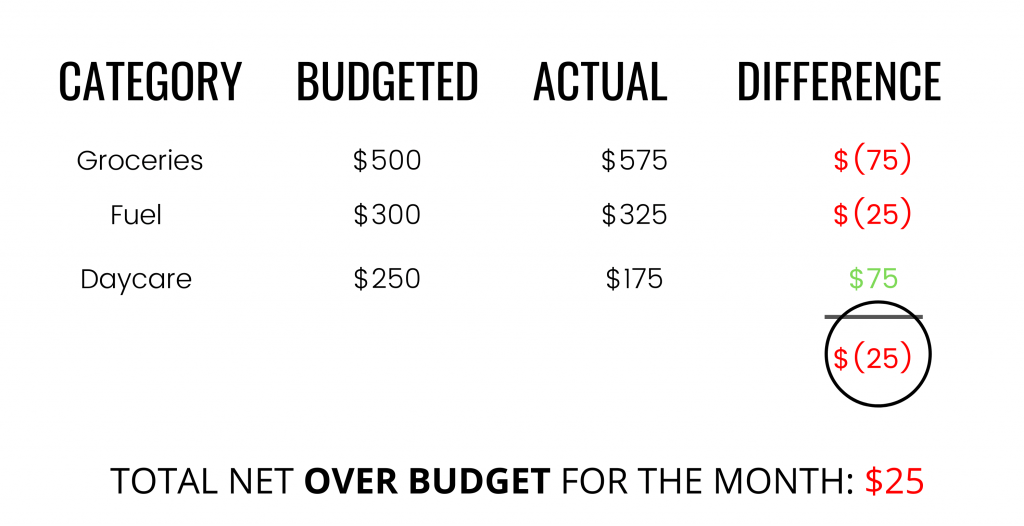

KEY CONCEPT EXAMPLE 2: RECONCILE BUDGET BALANCE TO BANK BALANCE (MONEY IS FINITE)

Let's say that you did pretty good on sticking to your budget for the month, but you had some discrepancies.

For simplicity sake , we will only look at a couple budget categories and assume on the rest you were spot on.

In this example, you're only $25 over budget, not a big deal. However, if you budgeted $2,000 of cash coming in for the month, and you end up spending $2,025, when your next paycheck comes (let's say it's $1,000), your bank balance will only show $975.

If you create your budget for the next paycheck based on $1,000 and forget the amount you were over budget from the prior month, you'll wind up $25 over budget again (considering you were spot on with all your budget categories).

Can you see how this snowballs? Pretty soon, you'll be wondering why your budget isn't working and here's why.

When you're over budget in any given month, that amount that you overspent doesn't just disappear and you have a clean slate the next month.

You actually, physically spent more money than what came in.

To fix, you can either start your next budget with $25 less than what you expect to earn, or pull from a sinking fund.

GETTING STARTED WITH BUDGETING

In order to create a budget you can stick to , you need to actually create a budget!

I have tons of budgeting resources that I've created to help you (FINALLY!!) take control of your money.

Here are some templates perfect for getting started with budgeting:

If you're wondering when the right time is, it's now, friend!

Trust me, if you're stressed about money now, you'll be more stressed later.

Once you perfect and create a budget you can actually stick to, you'll feel a weight lifted off your shoulders.

Don't fall into the trap of neglecting your finances, take control now and pursue financial peace.

Share this post!

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

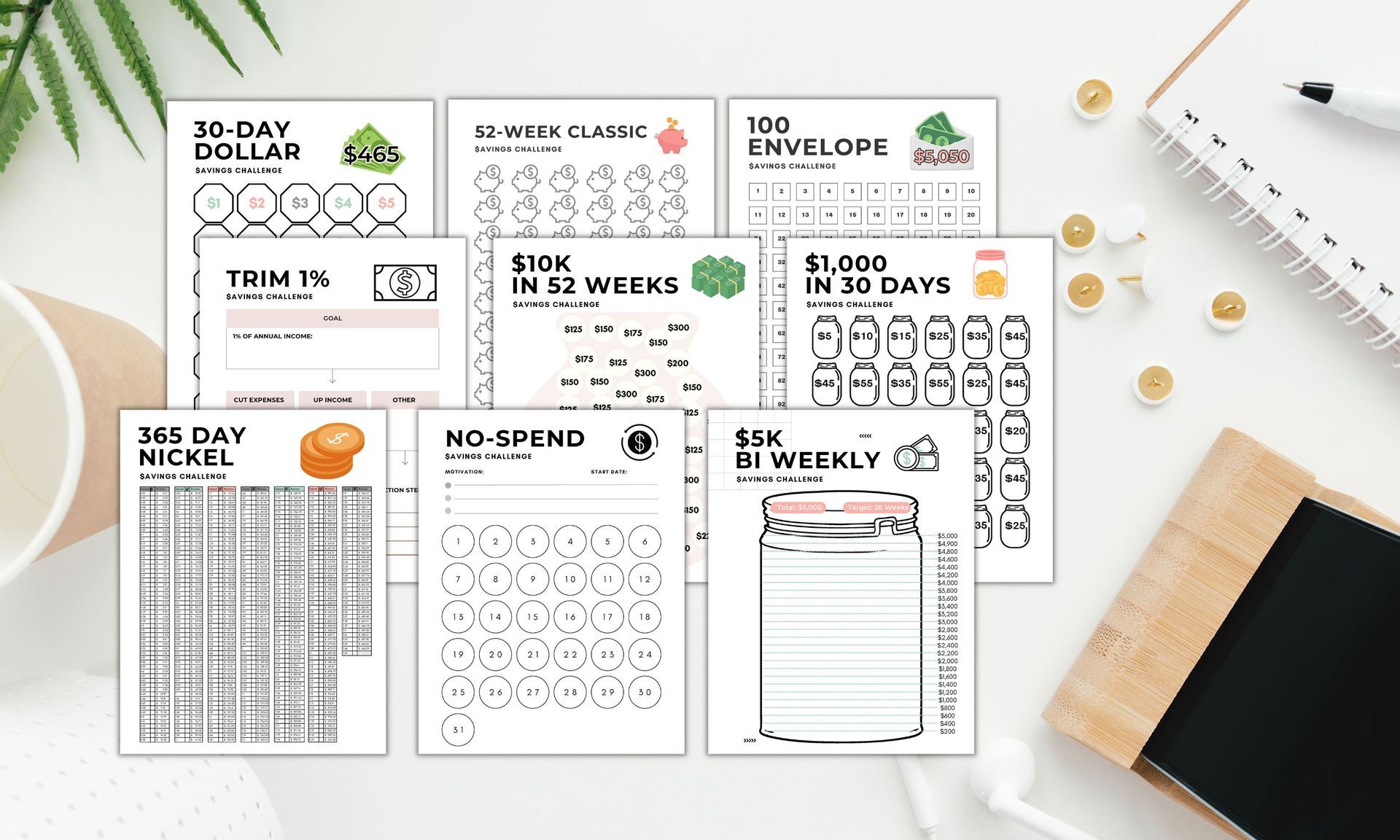

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!

Step by step tutorial how to make a budget in excel or google sheets. Plus, get my free google sheets budget template that can be exported to excel in just a few clicks! Creating an excel budget will save you time and make budgeting a seamless process.

How much to spend on housing every month is a burning question every homebuyer asks at some point. Here's what you should consider before purchasing a home and how to determine how much you should spend on housing every month in relation to your income.

When it comes to investing, time is the most important factor, as you can see from this example. Even though one invests only $100/month, she still comes out with more than the other two who invested over double what she did, just starting later! Even if you can’t invest much, do what you can 👏 #investing #investingforbeginners #investing101 #personalfinanceforwomen

Sharing our personal #budgeting formula for success! This is what we do every single month when budgeting finances. The KEY is to put financial goals before discretionary spending. The order you budget in is super important! Most people put wants and necessities first, don’t track their spending closely, then tell themselves if they have extra they’ll try and put some money towards financial goals. The only problem is there usually isn’t much extra! #financialliteracy #financialfreedom

If you want to buy a home in today’s real estate market, you’re going to need some home buying tips! You want your first home (or second or third) to be a blessing, not a burden. Many Americans are living paycheck to paycheck, and a home will not be a blessing if you can’t afford to miss a paycheck. With home ownership comes lots of financial responsibility, so you want to have a good grip on your personal finances BEFORE making the purchase!

Some things we did before we bought a home to prepare include:

• Did NOT base how much house we could afford on what the bank said we could. We used a much more conservative max price.

• Created a mock budget with all the added costs of home ownership- home repairs, renovations, property taxes, maintenance, etc.

• Bought the cheapest home in the most expensive neighborhood we could find (it’s all about location, location, location).

• Left lots of margin in the budget for expenses we knew we’d have down the road- like vehicle replacements, children, renovations, me being a stay-at-home mom.

Those are just a few of the things we did to ensure that we had a good grip on our finances before making the purchase. We didn’t want to be overwhelmed and stressed about money all the time because we over-extended ourselves financially with too much mortgage (also called being house-poor).

Fun fact: our monthly rent right before purchasing our home was $500/month. Man do I miss that… but I don’t miss the apartment!

Sharing our 25 budget categories for our family of 5!

Some of these are sinking funds (indicated on slide 2). Our monthly budget is constantly changing and having to be tweaked as our kids get older (and as we’ve added more to our family).

Got questions? Ask below!😌

#budgeting #budgetingfinances #personalfinanceforwomen #familybudget #budgetwithme #budgetwithmel

11 budgeting tips for beginners! If you’re new to budgeting and not sure where to start or you’re having trouble sticking to your monthly budget, give these tips a try! #budgetingtips #budgetingforbeginners #personalfinanceforwomen #financialfreedom #financialliteracy

How to #budget when you’re living on a #lowincome ✅ use these tips to help you increase your income and cut your expenses to break the #paychecktopaycheck and debt cycle! #personalfinanceforwomen

Buying a home can be incredibly stressful if you don’t prepare correctly! You want your first home to be a blessing, not a curse, and you want to avoid being house poor at all costs.

This is how to save for a home and some *general* guidelines to help you determine how much house you can *actually* afford (not just what the bank tells you you can) 🫠

The bank does their lending based on 40-50% of your take-home pay, which (to me) is crazy, and would cause me a lot of financial anxiety!

#buyingahome #savingforahouse #mortgagetips #personalfinanceforwomen #financegoals

Financial goals are essential to taking control of your personal finances, and hear me out—

SMALL GOALS ARE STILL GOALS AND A STEP FORWARD.

Everyone is going to have a different starting point. Saving $1,000 a month towards retirement might not be realistic for you right now, and THATS OKAY 👏

Half of achieving your goals is just setting them.

Set a big-picture goal, then break it down into bite-size chunks. If we don’t set small action steps, we can easily be discouraged and get off track.

When we first got married, our big-picture goal was to pay off all our debt. It seemed impossible— we were living on one income, cash-flowing my husbands final year of school, and I was entering an incredibly exhausting, busy tax season.

So we broke it down into small,action steps. We’d have to have a bare bones budget, and we’d have to live on HALF of my income. HALF. We set the goal— taped it to the fridge, and started.

Wouldn’t you know— we did it in half the time we thought it would take!

Set the goals. No matter how small they seem.

“And let us not grow weary of doing good, for in due season we will reap, if we do not give up.” Gal 6:9

Work like it all depends on you, pray like it all depends on God (because it does) 🤍

#moneygoals #financialfreedom #financialgoals #personalfinanceforwomen #personalfinancetips

Do you ever feel frustrated when unexpected, non-monthly expenses come up and blow your monthly budget? This is how we save for those irregular “gotcha” expenses, and ones that you just forget about.

When it comes down to it, though certain expenses are unpredictable in that you don’t know EXACTLY when they’ll happen, but you do know its likely they’ll occur— like it’s likely at some point your house and vehicles will need repairs, you just don’t know exactly when.

Make a list of all the non-monthly, irregular, seasonal & unexpected expenses that come up in your finances. It might be helpful to review bank statements to help you identity them.

Then, break each expense into a monthly amount and put it in the budget!

#sinkingfunds #financialliteracy #budgeting101 #personalfinanceforwomen #expenses

When we first got married, we had a mound of student loan debt to overcome. We were living on one income. We started Dave Ramsey’s debt snowball plan and were able to pay off over $20k of student loan debt in 12 months, by sending over 50% of our paychecks towards the student loan debt. Monthly payments no longer eat our income, we are free! This is how we did it. #payoffdebt #debtfree #debtfreecommunity #personalfinanceforwomen #studentloans

Practical budgeting tips for beginners! Discouraged by budgeting? Implement these budgeting hacks to create a monthly budget you can actually stick to & that allows you to reach your financial goals! 🎯

📌Save for later!!

#budgeting #budgeting101 #financialliteracy #personalfinanceforwomen

My new website is LIVE✨🎉

Over the last few months, I had my website completely redone and rebranded!

I’m now Budget with Mel 💁♀️ it seems a lot more fitting!

I can’t wait for you all to see the new site and follow along 🎈

#personalfinance #personalfinanceforwomen #budgeting #budgeting101 #financeblogger

🎉📣Major Announcement!! I’ve been keeping a secret…

My blog/website and all social media channels are getting a COMPLETE rebrand and totally new custom design!!

My new site will be much more user-friendly— easy to navigate and find what you want, easy to find freebies, and just sort through blogs and all my content in a much cleaner way!

Another major announcement may be following soon… keep your eyes peeled🙃

So excited for this much needed update and I will be sharing when it goes live!

Thanks for being here 😌

Texts from my mom😂 had to get on this trend. The accuracy once you have kids😜 anyone else?? #trendingreels #textsfrommymom #momreels #financeblogger #moneyblogger

This is my unconventional but effective budgeting formula🙌

Here’s a breakdown of each expense type listed:

- Necessities: food, housing, transpiration, utilities, insurance, etc. These are actual necessities— Netflix subscriptions don’t count! These are the expenses you would keep/have to pay in the event of a financial crisis.

- Financial Goals: these are “expenses” you put in your budget based on your long-term financial goals. For example, if investing 15% of your gross income is a goal you have (one I highly recommend), and you make $6,000 gross every month, you’d put $900 for investing in the budget. The KEY is that goals are immediately after necessities— they are non-negotiable!

- Discretionary: these are all your wants (vs needs). Think restaurants, clothing, recreation, extracurricular activities, subscriptions, etc.

- Irregular/Seasonal: these are expenses that are non-monthly, but probable. Think “gotcha” expenses. What expenses come up every couple months that cause you stress? Car repairs? Home repairs? Annual insurance premiums you forget about every year?! Instead of trying to cash flow them all in one month, set aside money for them every month. This way, when these expenses hit (its not if but when), you have the cash ready to go — or at least a good start!

Budgeted income - budgeted expenses should always total ZERO for a true zero-dollar budget ☑️

#budgeting #financialfreedom #budgetplanner #financialliteracy #budgetingforbeginners #budgeting101

This is my favorite #budgetingforbeginners tip!

If you can relate to any or all of these, this strategy is foe you! 👇

- because you are paid more than once a month, you struggle to follow a monthly budget. Your timing/cash-flow always seems off.

- you like to break every plan/goal down into small action steps.

- you struggle to stick to a monthly budget!

A paycheck budget is a specific budget strategy where instead of budgeting once a month, you budget every time you are paid.

A paycheck budget doesnt mean you’re living #paychecktopaycheck (though its great for breaking that cycle too). Rather, its just a detailed way for budget nerds like myself to make it easier for myself to actually stick to the #monthlybudget and track it throughout the month.

For certain budget categories, I like to break them down into weekly or bi-weekly amounts. For example, our monthly groceries budget is $400, so I break that down into $200 out of paycheck 1 & $200 out of paycheck 2. Could I simply spend $400 on the first of the month and still be fine? Absolutely! But I’ve found that budgeting this way helps me stay on track!

Another tip- we only keep the amount of cash we have budgeted for each line item in our checking account— I transfer what we want to save IMMEDIATELY after we are paid to another account so that im less tempted to spend it on something else. Its simple, yes, but very effective.

We also have our IRA contributions auto-withdrawn. This keeps me disciplined and less likely to say “ahh we’ll just skip this month so we can buy ____ .”

Hope this helps! ✨

This is how we have built wealth in our 20’s (against the cultural norm).

There’s nothing special about us, anyone can do it if you’re willing to delay your gratification and put in some work! Its not easy, but its with it. Once you start, these things become habits and they get easier to do as you go 👍

Your personal finances are SO SO important— how you handle money today will affect the dreams you can turn to reality, the legacy you leave your children (they’re watching and more is caught than taught), the health of your marriage, your ability to quit your job when you want to (not work past retirement), and your dependence on the government.

As Christian’s, we know that we are mere stewards of the resources God has given us. Its ALL His, and we wan to manage it faithfully as instructed in the Word.

The Bible tells us a fool devours all he has, but a wise man:

1) leaves an inheritance for his childrens children

2) gathers money little by little

3) does not submit to worldly pleasures

4) uses his resources to cheerfully give to others

5) stays away from debt

Those are some powerful principles that we can apply as believers!

Here’s what we’ve been doing in our 20’s!

#personalfinance #financialliteracy #personalfinanceforwomen #moneymanagement #biblical #godlywisdom

This is what delaying #investing just 10 years will cost you! Sally started at age 25 instead of 35 like Amy, and she contributed $200 less per month than Amy and still wound up with nearly double Amy’s total!

My biggest pieces of advice for #investingforbeginners

✅ just start

✅ set up an auto withdraw

✅ utilize a Roth IRA

✅ stop putting it off — you’ll never feel like its the “perfect time”

#financialliteracy #personalfinance #investing101 #investingtips

When you’re out to dinner with your husband and he catches you calculating how much you can save if you skip an app and extra cheese 🧀 #personalfinance #personalfinanceforwomen #moneysaver #financeblogger #frugaltips #cheapskate

Do you feel defeated because any time you try to commit to budgeting, saving money, investing, etc., unexpected expenses always pop up during the month and blow your plan?? You need sinking funds!

Follow the steps in the reel to save money and beat unexpected expenses 👊

These are sinking funds we have RIGHT NOW:

☑️ car repairs

☑️ home renovation

☑️ medical (in an HSA)

☑️ new tires

☑️ vehicle replacement

☑️ vacation

☑️ Christmas/holidays

☑️ gifts

☑️ annual insurance premiums

☑️ meat (purchase a steer)

Sinking funds we’ve had in the past:

☑️ maternity leave

☑️ baby (HSA)

☑️ new furniture

☑️ baby equipment/gear (non-medical costs)

Sinking funds are a game-changer ✨

#sinkingfunds #budgetingtips #budgeting #personalfinance #personalfinanceforwomen #financialliteracy #financetips

Does the current stock market scare you? Here are 4 do’s and Don’ts when the stock market is down 📉

✨Bonus: split your investing portfolio between these 4 mutual funds 👇

- growth

- growth and income

- aggressive growth

- international

#financialliteracy #personalfinanceforwomen #investingforbeginners #stockmarketinvesting #investingtips #investing101

People will try to give you all kinds of shovels to dig yourself into a hole— a debt hole. That hole sets you back financially for years! There’s the car debt shovel, student loan debt shovel, credit card debt shovel. Many young people have even said that they’ve put off marriage, kids, and buying a home because they’re in so much debt.

Additionally, whenever the Bible talks about debt, it’s never in a positive way. It warns against being a co-signer, and compares debt to slavery.

In a nation where broke is normal (70% of people are living paycheck to paycheck), sorry, count me out ✌️

👉I don’t want to be dependent on my next paycheck to make ends meet.

👉I don’t want to use a credit card as a lifeline to fill the gap between income and expenses every month.

👉I won’t advise my kids to pay $120k for a 4-year degree, pay interest on that $120k, delay marriage and a family, and be a slave for 20+ years to the lender just to get a piece of paper that is the “gold standard” of approval for entering the workforce. Especially when their father got a 2-year trade school degree and comfortably supports a family of 5 🙊 (can you tell how I feel about higher Ed??🤣)

We don’t have any car debt, student debt (anymore), and we have no credit cards to our name.

This forces us to be intentional, self-disciplined, and to weigh every purchase we make carefully.

No, I don’t think consumer debt is ever a good idea!

What’re your thoughts??

#financialliteracy #consumerdebt #debtfreecommunity #payoffdebt #debtfree #studentloans #creditcard #carpayment

Checking your account balance is not the same thing as budgeting! A budget is a plan for every dollar, on paper, before the month begins. While for some people simply checking your balance might work for a while, it’s a plan that only works in the good times. You need a plan that works in the good AND bad times.

#financialliteracy #budgeting #financetips

“If you knew what the government did to your money, there would be no federal reserve.” #endthefed #economics #economictimes #inflation #financialliteracy #biggovsucks

“No discipline seems pleasant at the time, but painful. Later on, however, it produces a harvest of righteousness and peace for those who have been trained by it.” Hebrews 12:11

Did you catch the last part of that verse? Discipline, though painful, will later on produce a harvest IF you have been trained by it. That’s a big if.

Sometimes we make the mistake of after we do something big and change our life in a big way, we think we are owed or deserved something.

For example, we paid off all our consumer debt in 12 months while living on one income. Wow! Great! It was super super hard, and required a lot of self-discipline and determination to persevere and stay motivated.

But you know what the actual really hard part is?

Now that we’re debt-free (besides our mortgage), we are able to take our foot of the gas a little bit. Diligently save and invest, but also enjoy life.

The hard part is CONTINUING to consistently do the same thing over and over again — save up for large purchases, invest 15% of our gross income, always pay cash (no credit cards).

You see, we COULD spend more on groceries, we could take more vacations, we could do more shopping. Drive a fancier car.

But for us, we have long-term goals that we believe will pay off more and are worth the work of planning meals, price comparing, and saving up month after month to pay cash for everything.

Because $200/month could make you over $1 million dollars if invested consistently for 40 years and not touched.

The small things matter. No, they may not make or break your ability to build wealth in one month, but they do matter. Because your BEHAVIOR and ATTITUDE about money matters.

The small choices you make reflect your habits, and if you want to change your life you have to change your habits. #financialliteracy #personalfinance #personalfinanceforwomen #moneymanagement #selfdiscipline

What happens if you #invest the average car payment?? You’ll #retireamillionaire ✅ This is why getting out of debt is so important— it eats your monthly income so there isn’t much left to save & invest!

If you invest $500 for 25 years starting at age 25, then leave it alone and don’t contribute a dime more from age 50-65 (15 years)— you’ll have over $1 million.

*Assuming a 10% average annual rate of return

Money management is something we all do, but how well we do it will determine how much financial stress and financial anxiety we feel surrounding our personal finances. These are ways you can take control of your financial future.

✨Build an emergency fund. Aim to save 3-6 months of expenses (not income) in a separate savings account. If you have a stable, predictable income, then you probably only need 3 months of expenses saved. If you have irregular income, or you are a business owner, commission employee, etc., you might want to save closer to (or even more than) 6 months expenses. This will help you survive financial crisis - job loss, major repairs, unexpected medical bills, etc. An emergency fund is an incredible safeguard that will help you sleep better at night.

✨Pay off all your debt. Debt is stressful. There’s no way around it. The best way to reduce financial anxiety surrounding debt is to pay it off. Aim to pay off all your consumer debt as quickly as possible using the debt snowball method- where you list your debts smallest to largest & pay off in that order. See Dave Ramsey’s website for more details.

✨Make a detailed budget, and stick to it. Budgeting finances is incredibly easy. Add your income, list all your monthly expenses, and budget it to zero. Be sure to allocate income to saving for large purchases and investing (or other financial goals).

✨Make both short & long term financial goals. If you don’t have goals, it will be hard to stay motivated to take control of your finances. Let’s face it— personal finances can be boring, especially if you’re a free spirit (not a nerd). If you make goals, it keeps you motivated AND the likelihood you’ll actually hit your goals goes up tenfold!

✨Automate your finances. Set up auto-withdraw for your bills (and savings!!), so that you aren’t tempted to brush them off and pay them later, only to forget and realize you don’t have enough money to cover the bill that month. You get behind little by little, small decision by small decision. Pay bills first, savings second, and spend what’s left over.

#financialliteracy #financialfreedom #financialstability #financialstress #personalfinanceforwomen

Why is college pushed as the ticket to a successful life? Why is institutional education considered the best education?

Call me old school, but I think your aptitude, skills, and personality are what set you apart.

My first two years of college was a literal repeat of everything I learned in high school. So I paid $60k for a “refresher.” They know this. But they got you- you have to have a certain number of “credits” to graduate, and there are certain requirements for what kinds of classes those can be at different universities. You’re in golden handcuffs.

Truth be told, I learned the majority of the tax code and tax return mechanics from PREPARING hundreds of tax returns my first year, and having a veteran accountant review and correct my work.

I realized after working just how little use my actual degree was. You learn by doing!

So ask yourself, as either a parent of a potential college student, or a college student:

1. How löng will it take me to break-even on my degree?

2. Do I really know what I want to do, or should I do some job-shadowing and work some different jobs first?

3. Can I find an employer who will train me instead of going to college for 4 years just to enter the workforce?

As I’m considering hiring a virtual assistant myself, I could care less if the person who I (potentially) hire has a college degree. I care about who they are as a person- their skills, personality, and willingness to learn. End of story. #entrepreneurspirit #degree #tradejobs #bachelorsdegree #collegedebt #collegedegree

My secret #budgeting weapon: the paycheck budget! Paycheck budget planning is not just for those living paycheck to paycheck, it’s for anyone who wants more control over their finances and a better method to stick to their monthly budget! #paychecktopaycheck #paycheck #budgetplanner #monthlybudget #financialliteracy #financialindependence #moneysavingmom #personalfinanceforwomen

Here are some ways you can save money on the rising cost of groceries! Some more info on how I’m saving money despite high (and still rising) inflation:

⭐️Some Top Ways I Save Money:

Stay out of the snack aisle. It will cost you double to buy single-serving, pre-packaged goods. While it’s convenient for kids lunches, buy the food item in bulk (or choose a healthier option), and put in reusable containers. You can even choose a day of the week to make 3/4 of your kids lunches or their entire lunch for the week and either freeze or refrigerate if necessary.

Price compare (quickly). While this sounds super simple (it is), I’ve found that sooo many people don’t realize there is a per unit price on most price stickers. Did you know that?? This makes it super easy to quickly compare what the cheaper item is per unit.

Buy staples in bulk no matter your family size. Even if you have a small family, buy in bulk. When it was just my husband and I, it didn’t seem effective to buy in bulk because we wouldn’t eat everything before it expired, and I didn’t realize how many things you could freeze (trust me, I knew NOTHING about food cooking, preservation, etc, etc).

Which brings me to point 4…

Freeze, freeze, freeze. Seriously. I freeze just about anything and everything. Cheese. Butter. Sour cream. Pancakes. Cream cheese. Fruit. Coffee (ice cubes). You name it, I freeze it. Buy the dairy mentioned above in bulk, then freeze. Take out of the freezer as needed so you don’t waste and let food go bad!

Commit to 1 grocery store trip/week or less. The more you go to the mall the more money you will spend. The more you go to the grocery store, the more money you will spend. This is more an act of self-discipline than anything else. If you commit to going only say once per week (you decide what’s doable for your family), and STICK TO IT, you will see a decrease in your spending. If it’s mid-week and you realize you’re out of something (that isn’t a necessity), find something at home to make. Get creative. This will force you to use what you already have on hand and PLAN before you go to the grocery store (both a meal plan and a shopping list).

If you’ve just started your #investing and #retirementplanning journey, it can be confusing trying to decide where the best place to invest your money is. Here’s how to invest for beginners & investing tips for everyone! #investingtips #investingforbeginners #investing101 #investingstrategy #rothira #401k #ira #retirementgoals #retireearly #personalfinance #personalfinanceforwomen

How to Invest for Beginners:

✨How much to invest?

Try to invest at least 15% of your gross household income into tax-advantaged retirement accounts. Do not include any employer match incentive for purposes of the 15% calculation.

✨IRA vs. 401(k)?

An IRA is an individual retirement account, where you invest money apart from your employer-sponsored 401(k) account. Think of an IRA as a DIY investing option, although I recommend using an investing professional from a brokerage firm to help you get started with an IRA. A 401(k) is tied to your employer, and typically has more limited investing options (the average has about 20 funds to choose from), and often times employers have an employee matching incentive.

✨Roth vs. Traditional?

Roth & Traditional investments are a TYPE of investment INSIDE your retirement account. These terms are specific to retirement savings accounts, not general investing accounts. Traditional contributions are made pre-tax, and both the principal and growth are taxed in retirement. On the other hand, Roth contributions are taxed on the way in, but both the growth and principal distributions are tax-free in retirement!!

Investing is a key part of #retirementplanning , but you can make so many mistakes, which deters many people from #investing at all. Don’t make these investing mistakes! #investing #investors #stocks #retireearly #retireyoung #investingtips #investingforbeginners #investmentstrategies #401k #ira #rothira

Don’t you dare come at me with “iTs BeCaUsE oF rUsSIA”, no it’s because of our energy policies 😬

C’mon, man.

#samsclub #keystonepipeline #drillbabydrill #gasprices #inflation #bidensucks #groceryshopping #grocerylist #grocerystore #economics #economy

Inflation is an invisible tax imposed on the people by a government, but how?

When they can’t get “their” money via ⬆️ taxes, they confiscate it by printing money and reducing your purchasing power.

If you knew the harm the Fed caused to your money, there would be no Fed. In promises of “fixing” and stabilizing the economy, they only make it worse.

Caused by:

✅ gov borrowing

✅ gov spending

✅reckless monetary policy

Governments have two ways of paying their expenditures:

▪️direct taxation

▪️ borrowing money — pushing the bill onto the taxpayers of the future, and todays taxpayer must pay the interest

The government isn’t really even borrowing and spending anymore— they are simply printing money out of thin air and spending… then forcing you to foot the bill via inflation.

At some point the brakes have to come on and there will be a reckoning, probably much worse than the 08-09 financial crisis.

This time may we learn from it. #inflation #government #taxes #tax #economics #economy #stocks #stocktrading #investment #investing #invest #monetarypolicy #federalreserve #interestrates

4 *must know* HSA benefits! 💡 Here’s why we choose an HSA over an FSA! #hsa #fsa #medicalexpenses #investment #investing #invest #healthsavingsaccount #flexspending #employeebenefits #savingmoney #healthinsurance

If you aren’t familiar with our story (why I started this account and my blog 4 years ago)… here it is! We paid off over $20k of student loan debt in 12 months while living on one income (my husband was still in school).

I started full-time work as a tax accountant when we got back from our honeymoon, and he was in school during the day and worked construction after school until he started his internship!

It was an incredibly busy first year of marriage! We worked our butts off to knock my student loan debt out in 1 year.

It wasn’t without struggles. During this time we :

- cash flowed our honeymoon

- cash-flowed a $5k car repair

- didn’t eat out, buy anything new, and lived in a janky apartment that was cheap and allowed us to send a lot of money to debt

Though difficult, this time helped us set a firm foundation to build our finances together— God’s way. We learned how to work together as a team, work HARD, sacrifice, and live well below our means.

The self-discipline and financial habits we developed have served us well.

We still don’t have any credit cards. We live well below our means. We don’t care much about what other people have. We’re content. We automate our investing. We pay extra on our mortgage because we just hate debt.

#payoffdebt #debtfreejourney #debtfreegoals #studentloans #studentloandebt #moneymindset #personalfinance #financetips #debtfreedom #debtsnowball #daveramsey #financialfreedom #financialliteracy #financialpeace

💡A Roth conversion is the process of transferring funds from a Traditional to a Roth retirement account.

The following scenarios would be a situation where a Roth conversion could take place:

1. Transfer from a Traditional 401(k) to a Roth 401(k). Example: Let’s say your employer adds a Roth option to their 401(k) plan. You decide to move the funds in your Traditional 401(k) to the Roth 401(k). The money never leaves the plan, it just changes nature of taxability.

2. Rollover from a Traditional 401(k) to a Roth IRA. Example: You leave your job where you have a Traditional 401(k). You roll over the funds from your old employer account to a Roth IRA— which is a retirement account separate from your employer sponsored plan.

3. You convert a Traditional IRA to a Roth IRA. This most commonly happens when someone exceeds the income limits of being able to contribute to a Roth IRA. Example: You make too much to contribute to a Roth, so you open a Traditional IRA. You contribute all year to the Traditional IRA, then convert it to a Roth IRA at the end of every year.

🔑The main difference between a Roth retirement plan & a Traditional retirement plan is WHEN and HOW they are taxed.

💡You contribute money to a Roth retirement account AFTER-TAX, but the GROWTH on the contributions is not taxed.

💡You contribute money to a Traditional retirement account PRE-TAX, and the GROWTH AND CONTRIBUTIONS are taxed in retirement.

Depending on your situation, this can make a big difference. Some general principles:

- If you’re young, you’ll likely want to contribute to a Roth. If you have 30-40 years of growth, you want that growth to be tax-free!

- If you expect your income to go up, you’ll likely want to contribute to a Roth (when you have the lowest tax rates you’ll have in your working years).

NOTE: Regardless of whether you have a Traditional or Roth 401(k) option at work, the ER match portion of your retirement savings is ALWAYS taxable.

#retirementplanning #retireearly #retireyoungretirerich #rothira #401k #ira #investing #investingtips #investingforbeginners #financialfreedom

“TaX tHe RiCH”🥴 as a former CPA, this one just gets to me. Did you know that businesses pay 93% of all income taxes — which then, lowers employee wages & prices as income tax burden rises? The U.S. has one of the most progressive tax systems in the world. People like to point to the Scandinavian countries as the “perfect model” because they have lots of social programs, but when it comes to taxes, they are MORE capitalist than the U.S. — everyone pays a flat tax (my personal preference). When businesses are allows to thrive, workers thrive, the economy thrives, and everyone is better off. #taxseason #taxtips #taxtherich #economics #economics101 #capitalism #socialism #socialismsucks #politics

Thanks but no thanks. Everything requires a spreadsheet. My budget, my grocery list, each child, EVERYTHING 🤗 #spreadsheets #nerd #accountinglife #accountant #cpa #accountinghumor #excel #microsoftexcel #spreadsheet #budgeting #budgetplanner #familybudget #momsonabudget #budgetingtips #personalfinance #moneymanagement

⚠️ Unpopular opinon alert…

I believe today’s generation of parents participate in a form of child welfare by not teaching their kids the value of hard work. Any discomfort or challenges their children face are immediately removed.

I wouldn’t be who I am today if it wasn’t for my parents and the lessons, both direct and indirect, they taught me about money.

We had to work, and work hard. My parents were not interested in being our personal ATM. They provided the necessities, we worked for everything else, starting in middle school!

You can teach your kids about money at every age, here are some ideas to get your started!

➡️ For all kids:

✔️ More is caught than taught. Model smart money behaviors yourself first and foremost.

✔️Pay commissions, not allowances. Never once in my life did I have an allowance. I survived. My parents paid commission to show us that you have to work for what you want AND need.

✔️Establish chores that aren’t paid, but are just required for being part of the family.

✔️ Cut them off when they graduate.

➡️ For smaller kiddo’s:

✔️Keep a jar of coins to show that you don’t waste things and small contributions add up over time.

✔️Explain to them WHY they can’t have something. For instance, reasons could include- you already have one at home, life isn’t always fair, or it’s not in the budget right now.

✔️Have them re-use items year to year. This is a great idea for school supplies! If they already have a perfectly useable backpack, binder, pencil box, etc, have them re-use these items.

✔️For really young kids, keep jobs/chores short and simple.

✔️Pay your child immediately after the job is done to teach them the relationship between work & money.

These are just a few ideas! Follow along for more tips 💥

‼️let me know in the comments how you teach your kids to work‼️

#teachingkids #personalfinance #personalfinanceforwomen #personalfinancetips #familybudget #familyfinances #momonabudget #financialeducation #financialliteracy #daveramseybudget #workethic #hardworkpaysoffs #hardworkpays #familybusiness #raisingtoddlers #raisingteens #raisingtinyhumans #raisingthefuture

Are you relying on social security as a retirement vehicle? The SSA is projected to be insolvent by 2033. Benefits are expected to be cut, so you won’t even get out of the system what you put into it.

Sound like a good deal? 🙅♀️

The U.S. government thinks you are not capable of making your own financial decisions, so they forcibly take money from your paycheck and do it for you via payroll taxes.

Some nuggets of info about social security:

1️⃣Social security benefits are comparatively lower than market rates of return. You can even have a negative rate of return after adjusting for inflation. The unrestricted free market ALWAYS outperforms government run social programs. The stock market has averaged a 12% rate of return since it’s inception.

2️⃣If you die before reaching government-regulated retirement age (another discussion for another day), you lose all your Social Security benefits. If you invest privately, you can ensure that if you die the money you have diligently saved can be passed onto someone close to you. Hows that for a deal? They will take money you could’ve been investing, invest it for you, and then if you die, they keep it.

3️⃣Social security benefits are subject to double taxation. You are taxed on your gross (W-2) income, which includes the money that was remitted to the gov for social security taxes. Then, in retirement, you are taxed on your benefits if you earn over a certain amount in retirement, and the income levels are not very high (it’s almost like you’re being disincentivized from earning money in order to enjoy retirement).

How’s that for a good deal?

In the name of “compassion” the government tries to act as a white horse saving the day. However, when you read between the lines, you realize that what you are giving in exchange for what you are getting is not a good deal 👎

Alright, queue all the commies sending me hate mail 😂

#socialsecurity #retirement #retirementplanning #retirementgoals #governmentspending #inflation #investing #investingtips #investing101 #investingforbeginners #economics #economy #freemarket #stockmarket #taxes #notaxationwithoutrepresentation

Getting ready to see what you made before the government robbed you blind 🙄😅 #taxes #taxseason #government #incometax #socialsecurity #medicare #fica #paycheck #paychecks #january #federaltax

You’re shocked?? 😂 the average car payment in the US is right over $500/month… OF COURSE it feels like you have no money! #carpayment #debtfreejourney #debt #daveramsey #debtisdumb #cashisking #getoutofdebt #payoffdebt #usedcars #newcar #daveramseybudget #daveramseybabysteps #daveramseyplan #consumerism #consumerbehavior #consumerdebt

When the hubby says Chik-Fil-a doesn’t qualify as a “nice date.” 🤪

I’ll forever be the spender and he will forever be the saver🥰 that’s what makes it work!

If I didn’t have him, I’d never go out. If he didn’t have me, he’d never eat in😉

Are you the spender or saver?? Give me a funny story below about it 👇

#personalfinance #spender #saver #moneysaver #moneysavingtips #daveramsey #daveramseybabysteps #daveramseybudget #moneyandmarriage #money #savers #moneysaver #frugalliving #frugal #cheapdate #frugalmom #thriftymom

The best way to get rich quick is to get rich slow.

Here’s what you DON’T need to become a millionaire:

❌ Six-figure income

❌ College degree

❌ Luck

❌ Single stocks

❌ Cryptocurrency

❌ Real estate (although this can be a great source of passive income/investment once you are completely debt-free)

This is what you DO need to become a millionaire:

✅ Consistency - investing every month over a long period of time. There is no shortcut to wealth. The best way to get rich quick is to get rich slow.

✝️ Proverbs warns:

“A faithful man will abound with blessings,

but whoever hastens to be rich will not go unpunished.”

✅ Discipline - you have to discipline yourself to pay yourself first and be willing to make sacrifices NOW so you can reap the rewards LATER.

✅ Live on less than you make - you can never out-earn bad money management.

If you invest just $200/month consistently for 40 years, with an average rate of return of 10%, you will have $1,264,815 in retirement!

You might think, 10%?? Yeah, right. No one makes that good of a return on their money unless they get lucky and invested in a business early on that went big (think Walmart, Microsoft, Apple). This couldn’t be further from the truth. That accounts for MAYBE 1% of investors. Most people become millionaires by cultivating the habits I outlined above.

Since inception in 1926, the S&P 500 has averaged right at a 10% rate of return.

Will you get 10% every year? Nope! Some years you might only get 3%, or you might simply break even when you account for inflation (hello 2021/2022!!). It’s all about staying the course - weathering the highs and lows of the market 📈

👉🏼Side note: The S&P 500 is just fancy terms for an index of 500 leading publicly traded companies in the U.S. So different companies are always being pulled in & out of the S&P 500 based on their performance. You should actually average higher than the S&P 500 if you have a good investment professional!

#investing #personalfinance #personalfinanceforwomen #investingtips #investing101 #investingforbeginners #investingstrategy #stockmarket #retirementplanning #retirementgoals #millionaireminds #daveramsey #daveramseybabysteps

💡Looking for a way to save money this year?

I talk a lot about this, because it’s so powerful — using cash literally changes how your brain responds to a purchase. The feeling associated with the purchase is more powerful.

Think about it— is it harder for you to hand over a Ben Franklin to the cashier or swipe your card?

Additionally, If you commit to using cash for certain budget categories, you can leave your cards in the car and this way you force yourself to only spend what’s in the envelope— it’s your only option that way! 📩

I won’t go into all the research for this specific post that shows willingness to pay doubles when a card is used, because I think most of us can admit we don’t think as much when swiping plastic vs handing over physical cash.

I sell these cash envelopes in my Etsy shop if you’re interested!

✅ 4 different floral designs

✅ customizable blank envelopes

✅ elegant design

✅ instant download

✅ over 25 pre made envelope categories

Here is the link if you’re interested:

💫Vertical envelopes:

https://etsy.me/34amnxp

💫 Horizontal envelopes:

https://etsy.me/3zKRlrX

#personalfinance #cashenvelopes #cashenvelopesystem #cashisking #debtisdumb #daveramseybudget #cashenvelope #cashenvelopestuffing #frugalliving #budgetmum #financetips #financegoals #moneysaver #moneysavingmom #moneysavingtips #savemoneytoday #savemoneylivebetter #moneymanagement #frugalmom

These DM’s always irk me. The “must be nice to _____.”

And they’re always from people who don’t know anything about me besides that we paid off all our consumer debt in 1 year & I quit my job as a tax accountant to stay home with my kids.

Based on this set of facts, the assumption is that I

- came from a wealthy family which set me up for success

- make insane amounts of money

- have never had any hardships

None of these are true. But that doesn’t matter to people who assume that success comes from luck (marrying into money, growing up wealthy, receiving an inheritance, etc.)

Did you know that over 90% of Americas millionaires are self-made & never inherited a DIME?

Bet CNN won’t tell ya that fun fact🙃

The TRUTH is:

✅ I paid my way through college, working 3 jobs (before classes, in-between classes & after class)

✅ I did NOT grow up wealthy

✅ My husband & I paid off all my student loans while living on one (modest) income

✅ I drove a beater for 6 years until getting our minivan in 2018

✅ Today we still make many sacrifices to save, invest, and build wealth

So no, I haven’t had it “easy” , but that’s relative. I’ve had it easier than some, and worse than some.

#personalfinance #personalfinanceforwomen #financialfreedom #financialliteracy #payoffdebt #debtfreecommunity #debtfree #debtfreeliving #daveramsey #daveramseybabysteps #studentloans #millennialmoney #moneymanagement #financeblogger #debtisdumb #cashisking #debtsnowball #debtfreegoals #financialgoals #moneygoals #2022goals

Debt is one of the most normal things in the world to most people. The government subsidizes it(via tax breaks and being in the student loan business), many parents encourage it (student loans), and Americans buy it.

🧑🎓The average student loan debt is just over $37,000.

💳The average balance on a credit card is $5,525.

🚗 Americans borrow an average $34,635 for new vehicles and $21,438 for used vehicles.

I think part of the issue is we lack contentment, and part of the issue is we lack knowledge.

✨People don’t take the time to calculate how much they’ll end up paying in total (after interest) for their degree, new car, furniture, etc.

✨Most don’t realize that credit card companies spend billions on consumer behavior research every year, so when they offer you cash back & airline miles, they know they’ll more than recoup their costs by the increase in your spending using credit instead of cash or debit (it literally affects your mind differently).

✨Another one that will get me in trouble… a college degree is not a prerequisite for success! Trade jobs are sitting open, paying $45/hour starting wage, while students line up at the university to pay $100k for a degree that will put them at a lower starting wage than the trade job.

Getting out of debt was an incredible weight lifted off of our shoulders. It took a lot of sacrifice — we didn’t go on vacation or eat out, we rented a janky apartment for cheap, worked, worked, and worked some more, drove old, rusted, duct-taped vehicles, and ate a lot of beans and rice until we clawed our way out.

There is a better way, but you have to be willing to do the work! 💪

#personalfinance #personalfinanceforwomen #payoffdebt #debtfreecommunity #debtfreejourney #daveramsey #personalfinancetips #getoutofdebt #debt #debtfree #finance #financialfreedom #financialliteracy #cashisking #debtfreeliving #debtisdumb #millennialmoney #frugalliving #budgetmom #momonabudget #studentloans #credittips

**MY PERSONAL OPINION**

But it’s backed by research 🙃🙃

Do you honestly think you’re outsmarting credit card companies who spend BILLIONS of dollars on consumer behavior research??

Do you really think they’re giving you free money (“cash back”) without getting something in return?

They KNOW that their billions spent on research shows that you SPEND MORE MONEY with a credit card than a debit card or cash 👍

The buy now pay later mentality affects your purchasing decisions. Specifically, it affects your willingness to pay.

Let me give an example.

In one study, randomly selected participants were offered the opportunity to purchase tickets to an actual professional basketball game. They were either to pay by cash or credit card. They were asked how much they were willing to pay for those tickets, and those who were told they would have to pay by credit card were willing to pay over TWICE as much as those who were told they would have to pay with cash.

What’s going on here?

Payment method affects consumer spending behaviors.

The same study found:

👉 people pay less attention to prices when using a credit card

👉 it hurts the brain more psychologically to use debit or cash vs credit

👉 people who use credit cards are less likely to have a household budget

The facts don’t lie ✅

👉Source: Journal of Consumer Behavior

#financialfreedom #finance #financialliteracy #payoffdebt #debtfreecommunity #debtfreejourney #daveramsey #personalfinanceforwomen #millionairemindset #daveramseybabysteps #debtsucks #cashisking #personalfinance #creditrepair #creditcarddebt #creditcard #cash

🚗 What happens if you invest the average U.S. car payment??

👉 $550/month ( Yikes‼️)

👉 40 years (age 25 to 65)

👉 10% average annual rate of return

$3,478,243 in retirement ✔️

Don’t buy (literally and figuratively) the myth that you HAVE TO have a car payment, or that it’s smart!

If you’d take that car payment and invest it instead, you could be a millionaire.

Drive what you can afford, which is what you can pay cash for!

#carpayment #debtfreecommunity #debtfree #debtisdumb #invest #investing #stockmarket #compoundinterest #financialfreedom #financialliteracy #personalfinance #personalfinanceforwomen #personalfinancetips #moneymanagement #millennialmoney #daveramsey #daveramseybabysteps #debtsnowball #debtfreegoals #debtfreeliving

Do you ever wonder what percent of your income you should be allocating to certain budget categories? These are Dave Ramsey’s recommended budget percentages for your personal finances!

1. Giving 10%

2. Saving 15%

3. Housing 10-25%

4. Food 5-15%

5. Transportation 10-15%

6. Clothing 2-7%

7. Health 5-10%

8. Insurance 10-25%

9. Recreation 5-10%

10. Personal 5-10%

11. Debt 5-10% (+ any extra, pay off all consumer debt before investing)

#daveramsey #daveramseybabysteps #daveramseybudget #daveramseyplan #personalfinance #personalfinanceforwomen #financialfreedom #finance #financialliteracy #budgeting #budgetplanner #budgetmom

Just because there is high inflation doesn’t mean you can’t build wealth! These are 5 things we’ve done to deter inflation and build wealth this past year. Tips for combating inflation in your personal finances!

1. Made extra mortgage payments.

2. Invested in the stock market (mutual funds) so our money at minimum keeps up with inflation (hopefully outpaces it).

3. Kept our emergency fund on the low end. Put as much savings as we could in the stock market instead (for example our new vehicle savings is in a brokerage account instead of a savings account).

4. We haven’t made any major changes to our monthly budget (increases).

5. We don’t panic. Slow, steady, calculated, unemotional investing is how you win with money. The best way to get rich quick is to get rich slow ⭐️

#investing #inflation #personalfinance #personalfinanceforwomen #investingforbeginners #investing101 #investingtips #moneymanagement #moneymanagementtips #financetips #stockmarket #payoffdebt #payoffmortgage

When people try to justify the $70k 2022 suburban they can’t afford because it’s “for the kids safety”🤔

‼️I have nothing against suburbans or nice cars ‼️My only beef is when they’re used to justify a car payment that you can’t afford 🙅♀️

Once we had 2 kids in tow, we ditched my 2004 Ford Escape for a 2020 Chrysler Pacifica minivan that we bought used with cash!

The average car payment in America is over $500 🤯 that can be a major budget killer depending on your income! Save up, pay cash 💰

#personalfinance #debtfree #daversmsey #payoffdebt #debtisdumb #cashisking #carpayment #autoloan #debtsnowball #debtfreeliving #debtfreegoals #millennialmoney #getoutofdebt #payoffdebt

Had to do it 😂 I had way too much fun making these 🙃

But for real… SAVE THE GIFT BAGS BEFORE I LOSE MY SANITY THEY COST MORE THAN THE GIFT ITSELF 😆

I’m the psycho whose saving all the gift bags, wrapping paper, and tissue paper #frugalmom

I can’t help it. It’s my identity.

Merry Christmas Eve, God bless you & your family 💕

#personalfinance #personalfinanceforwomen #money #frugalliving #frugalchristmas #christmassavings #millennials #memes #christmasmemes #mommemes #funnymemes #daveramsey #daveramseycommunity

When you’re Christmas shopping and the cashier tries to convince you to open that store credit 🚫🙈

✌️not in a million years

We have never had a credit card in our 6 years of marriage, sorry not sorry 😉

We pay cash for EVERYTHING, because I know the research that shows your willingness to pay increases 150% using credit va debit or cash 👍 so save 20% today and spend 150% more on all future purchases! No thanks.

Felt like rufflin some feathers this eve of Christmas Eve 🎅

#creditcard #creditcarddebt #daveramsey #daveramseybabysteps #daveramseybudget #frugalliving #debtfree #personalfinance #personalfinanceforwomen #moneymanagement #holidayspending #cashisking #payoffdebt #millennialfinance

✨DIY WINTER DRY SKIN BODY BUTTER✨

1 part coconut oil

1 part epsom salt

15-30 drops essential oil of choice

✅ non-toxic

✅ frugal

✅ minimal ingredients

This was one of my favorite things to use in the shower when I was pregnant! Extremely moisturizing! #diyremedies #diyrecipe #dryskin #bodybutter #diybodyscrub #nontoxic #diychristmasgifts #frugalliving #naturalcures #naturalremedies #dryskincare

🌱 How to choose the best stock mutuale funds! We follow Dave Ramsey’s advice exactly and put our money into four buckets of stock mutual funds:

1. Growth

2. Aggressive Growth

3. Growth & Income

4. International

The key is to diversify your investing portfolio to mitigate investment risk. Mutual funds is just a fancy term for a group of stocks. We personally don’t invest in any single stocks because the return over time is not favorable and it’s risky! We don’t want our hard earned money being gambled by investing in single stocks! #stocks #mutualfunds #investing #investing101 #investingforbeginners #personalfinanceforwomen #investingtips #daveramsey #retirementplanning #financetips #finance #personalfinance

5 SELF-EMPLOYED SMALL BUSINESS RETIREMENT PLAN OPTIONS💡Did you know you have options as a small business owner to invest, despite maybe not having the funds to start a traditional 401k plan for you or your employees? You can even take advantage of a Roth IRA! #smallbusinessowner #investing #401k #rothira #simpleira #solo401k #investingforbeginners #retirementplanning #retirementplans #retirementsavings

💡401(k) vs IRA: What’s the difference? Great question, let me answer! I’d recommend:

✅invest in your 401(k) up to your ER match, then open an IRA. Open a Roth 401(k) if available through your ER retirement plan.

✅ if eligible, max out your Roth IRA ($6,000 for 2022). If this still doesn’t meet 15% of your gross income, continue funding the 401(k), which is maxed out at $20,500 for 2022.

✅ if you are not eligible to open a Roth IRA because of income limits, open a traditional IRA & convert it to a Roth at the end of every year, paying the taxes on your contributions upon conversion. This is called a back-door Roth.

#investing #rothira #401k #401kplan #investingforbeginners #investing101 #investingtips #retirementplanning #retirementincome #retirementsavings #personalfinanceforwomen #personalfinances #ira

💡This is exactly why you need to start #investing in your 20s! Harness the power of #compoundinterest to #buildyourportfolio! TIME IS MONEY! #investing101 #investingforbeginners #investingstrategy #investingeducation #financialliteracy #financialplanning

These are 7 sinking funds you need in your monthly budget & how to budget for a sinking fund! #sinkingfunds #sinkingfundstracker #budgeting #personalfinance #moneymanagement #savingsgoals #savingsaccount

✅ A few reasons you need a ROTH IRA ASAP! Be sure if your employer offers a Roth 401(k) you are taking advantage of that option. Then, invest above and beyond your match in a Roth IRA (this is an individual retirement account, not employer sponsored). Between the two, if you’re eligible, you can contribute up to $19,500 per year. However, for the IRA, the max contribution is $6,000 per person for 2021 ($12,000 per married couple) ‼️#rothira #investing #401k #investingforbeginners #retirementplanning #retirementgoals #millennialmoney

Easy way to figure out what paychecks you will use to budget and pay for which bills! A paycheck budget does not mean you’re living paycheck to paycheck, rather, it is just a detailed schedule showing when funds will leave your account and how each paycheck is allocated! A simple budgeting method. Link to this template in my bio! #paychecktopaycheck #paycheck #paycheckbudgeting #budgeting #budgetplanner #budgetbypaycheck #plannerinserts #plannerinspiration

If you’re planning a wedding, it doesn’t have to be expensive and stressful. Here’s how to create a wedding budget from scratch and save money on your wedding! #weddingbudget #budgetwedding #weddingplanning

Do you know your net worth? When it comes to personal finance, net worth is a much better indicator of wealth than income. You can make a million a year and still be broke 🥴 if your spending is equal to your household income, you’re by definition, living paycheck to pqycheck. Give it a try, calculate your net worth in a few minutes! Share in the comments how it went (don’t have to share numbers of course)- but were you surprised? Motivated? Happy?! #networth #finance #personalfinance #investing #wealth #personalfinanceforwomen #personalfinancetips #moneymanagement

If you're an employee, you've likely heard the terms 401(k), IRA, Pension, etc thrown around, but maybe have no idea what they actually mean.

The WORST thing you can do as an employee is set up your employer-sponsored (don't worry- this is defined in the slides😉) retirement account, and then never look at it again, assuming as long as you make contributions, you'll be set for retirement.

Or, you might have a few things briefly explained to you, such as the difference between a pension & mutual fund, but you don't really know what's the better choice 🤷♀️

I'm here to help with all the confusing retirement jargon!

Here are some key things to remember:

✅ 𝐀 𝐑𝐨𝐭𝐡 𝐈𝐑𝐀 𝐢𝐬 𝐚𝐥𝐦𝐨𝐬𝐭 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐭𝐭𝐞𝐫 𝐭𝐡𝐚𝐧 𝐚 𝐭𝐫𝐚𝐝𝐢𝐭𝐢𝐨𝐧𝐚𝐥 𝐈𝐑𝐀. Though you contribute to it with after-tax dollars (unlike a traditional IRA where you contribute with pre-tax dollars & get a tax deduction in the year of contribution), the withdrawals you make in retirement are 𝐭𝐚𝐱-𝐟𝐫𝐞𝐞.

✅ 𝐔𝐬𝐞 𝐚 "B𝐚𝐜𝐤-𝐝𝐨𝐨𝐫 𝐑𝐨𝐭𝐡" if you are above the income limits for contributing to a Roth IRA. Just note you will have to pay taxes on your contributions upon conversion.

✅ 𝐏𝐞𝐧𝐬𝐢𝐨𝐧𝐬 𝐚𝐫𝐞 𝐫𝐚𝐫𝐞 𝐭𝐡𝐞𝐬𝐞 𝐝𝐚𝐲𝐬, 𝐛𝐮𝐭 𝐢𝐟 𝐲𝐨𝐮 𝐚𝐫𝐞 𝐨𝐟𝐟𝐞𝐫𝐞𝐝 𝐭𝐡𝐢𝐬 𝐨𝐩𝐭𝐢𝐨𝐧, 𝐈'𝐝 𝐚𝐯𝐨𝐢𝐝 𝐢𝐟 𝐩𝐨𝐬𝐬𝐢𝐛𝐥𝐞. They have limited investing options and don't perform well. PLUS, you have no control over the investing decisions.

✅ 𝐀𝐥𝐦𝐨𝐬𝐭 𝐚𝐧𝐲𝐨𝐧𝐞 𝐜𝐚𝐧 𝐨𝐩𝐞𝐧 𝐚𝐧 𝐈𝐑𝐀. This is a great option to invest above and beyond your employer-sponsored 401(k). You will likely have more investment options.

✅ 𝐁𝐫𝐨𝐤𝐞𝐫𝐚𝐠𝐞 𝐚𝐜𝐜𝐨𝐮𝐧𝐭𝐬 (𝐧𝐨𝐧-𝐫𝐞𝐭𝐢𝐫𝐞𝐦𝐞𝐧𝐭 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐚𝐜𝐜𝐨𝐮𝐧𝐭𝐬) 𝐚𝐫𝐞 𝐞𝐱𝐭𝐫𝐞𝐦𝐞𝐥𝐲 𝐟𝐥𝐞𝐱𝐢𝐛𝐥𝐞 𝐛𝐞𝐜𝐚𝐮𝐬𝐞 𝐲𝐨𝐮 𝐜𝐚𝐧 𝐩𝐮𝐥𝐥 𝐦𝐨𝐧𝐞𝐲 𝐨𝐮𝐭 𝐚𝐭 𝐚𝐧𝐲 𝐭𝐢𝐦𝐞 𝐰𝐢𝐭𝐡 𝐧𝐨 𝐩𝐞𝐧𝐚𝐥𝐭𝐲. However, they offer no tax-savings, so they are good for saving up for large purchases, but not a great retirement savings option.

⭐️ And of course, always contribute at least 𝟏𝟓% 𝐨𝐟 𝐲𝐨𝐮𝐫 𝐠𝐫𝐨𝐬𝐬 (𝘣𝘦𝘧𝘰𝘳𝘦-𝘵𝘢𝘹) 𝐢𝐧𝐜𝐨𝐦𝐞 towards retirement ⭐️

Literally all the time 😂 sorry, had to. Part of laying out a budget means forcing yourself to see the 𝐨𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐲 𝐜𝐨𝐬𝐭 involved with your purchases.

Money is about behavior more than it’s about head knowledge.

If you can change your behavior, you can change your life. This is nothing new. Just like if I’m frustrated because it FEELS like I have no time, one look at my weekly screen time report and I realize time isn’t the problem— it’s my behavior.

𝘖𝘶𝘳 𝘧𝘦𝘦𝘭𝘪𝘯𝘨𝘴 𝘥𝘰𝘯’𝘵 𝘢𝘭𝘸𝘢𝘺𝘴 𝘢𝘭𝘪𝘨𝘯 𝘸𝘪𝘵𝘩 𝘳𝘦𝘢𝘭𝘪𝘵𝘺.

You might feel like you have no money to save, but in reality if you cut back to eating out 2x per month instead of 4x, you’d have $100-$150 to save. Or, if you sold your brand new car and got a used, reliable car paid for in cash, you’d have $300-$500 extra per month because you don’t have a car payment.

Ask yourself, 𝘈𝘮 𝘐 𝘥𝘦𝘢𝘭𝘪𝘯𝘨 𝘸𝘪𝘵𝘩 𝘳𝘦𝘢𝘭𝘪𝘵𝘺?

Do you really have no money living in the wealthiest country in the world? Or, are you a slave to your money because your behaviors around money are irresponsible?

Don’t worry, I’m always here for your reality check 😉

➡️ This should blow your mind.

If you invest just $100/month from age 20 to 75, at an 𝘢𝘷𝘦𝘳𝘢𝘨𝘦 annual return of 12% (you could have a 1% year and a 30% year), you will have $7,103,877 at retirement 🤯

$100 dollars per month.

𝘓𝘦𝘴𝘴 𝘵𝘩𝘢𝘯 𝘢 𝘤𝘢𝘳 𝘱𝘢𝘺𝘮𝘦𝘯𝘵. 𝘗𝘳𝘰𝘣𝘢𝘣𝘭𝘺 𝘭𝘦𝘴𝘴 𝘵𝘩𝘢𝘯 𝘵𝘩𝘦 𝘵𝘰𝘵𝘢𝘭 𝘰𝘧 𝘢𝘭𝘭 𝘺𝘰𝘶𝘳 𝘮𝘰𝘯𝘵𝘩𝘭𝘺 𝘴𝘶𝘣𝘴𝘤𝘳𝘪𝘱𝘵𝘪𝘰𝘯𝘴.

The problem is most people don’t think it’s possible— so they don’t have a long-term plan for their money.

Couple that with the fact that we have a problem with wanting what our parents and grandparents have, but not wanting to do what it took them to get there— saying no, consistent investing & saving, living below their means, staying away from consumer debt, etc.— leads to most people having a victim mentality when it comes to their personal finances.

93% of America’s millionaires are self-made. Additionally, most of the 93% came from lower or middle class families.

It can be done, and it should be.

If you’ve never added it up, I dare you😉 we spent upwards of $500 per month eating out before attacking debt & budgeting (and kids)! A few nights of takeout a week, dinner out on the weekends, meet up with friends for drinks... what I THOUGHT we were spending vs what we were *actually* spending were two completely different numbers 😑 but that’s what happens when you don’t budget, you really have no idea 🤷♀️ and quick tip— your best guess is usually not accurate! #daveramsey #budgeting #budgethumor #budgetingtips #personalfinance #daveramseycommunity #debtfreecommunity #debtfree #moneyhumor #personalfinanceforwomen #personalfinanceformillennials

When you are budgeting, it’s nice to have something to gauge if what you’re budgeting is reasonable.

These are Dave Ramsey’s recommended budget category percentages.

Now, remember, these are 𝘨𝘶𝘪𝘥𝘦𝘭𝘪𝘯𝘦𝘴. I understand that some people have extremely unique situations, and for example, someone with a family of 10 is going to probably be pushing the grocery budget percentage limits!

This is why they are general guidelines, not absolutes. These guidelines are designed to keep you on track so you can make your money do what you want it to, rather than being a slave to it.

If you’re housing is taking up 50% of your take home pay, you’re likely feeling pinched — and for good reason! You’re house poor, meaning you’ve bought more house than you can afford, and thus you have a hard time finding money left over every month to save or give.

Likewise, if your grocery budget is taking up 25% of your take home pay, you might need to scale back the Costco trips and start meal planning to free up some of your income for other things.

➡️Swipe right to see some important notes on housing & saving in particular!

ITS A BIG DEAL 🤣 love my husband for these important reminders before I lose my mind reconciling our bank account!

I reconcile daily and I’m still off $10 sometimes. I try and figure it out for a few minutes and if I can’t, no biggie 🤷♀️ #bankreconciliation #accountant #personalfinance #personalfinanceforwomen #budgeting #monthlybudget #budgetmom

There is one baby step in Dave Ramsey’s FPU plan that we will not complete— funding kids college!

My husband and I carefully considered what we thought would be best, and ultimately came to the conclusion that we want our kids to take 𝐫𝐞𝐬𝐩𝐨𝐧𝐬𝐢𝐛𝐢𝐥𝐢𝐭𝐲 for their education.

The cost of higher education has risen dramatically over the last 10 years, and frankly, we are of the opinion that the value of the education has not increased proportionally. In fact, it’s decreased (we believe).

America is 𝘰𝘣𝘴𝘦𝘴𝘴𝘦𝘥 with credentials, but credentials don’t determine success, and everyone has to decide what success means for them.

41% of recent college graduates are working in jobs that don’t require a college degree.

High paying trade jobs sit empty while high schoolers are pressured into going to school or being labeled a failure.

But at what cost? 4-8 years of schooling is a long time, and the opportunity cost must be considered.

We will absolutely support our kids if they decide to go the college route, and advise them (if they’ll let us 😜) to find a school they can afford. This might mean working and paying their way to a community college, or if they’d like to attend a four year school, working REALLY hard to compete for scholarships!

Everything you need to know about the Advance Child Tax Credit from the American Rescue Plan Act (ARPA) ✅ #americanrescueplan #taxrefund #taxseason #childtaxcredit #advancechildtaxcredit #taxcredits #cpa #taxaccountant #taxreturn #presidentbiden #personalfinance #personalfinanceforwomen #financetips

•𝐒𝐈𝐍𝐊𝐈𝐍𝐆 𝐅𝐔𝐍𝐃𝐒•

So many people feel defeated by unexpected expenses that seem to come up 𝘦𝘷𝘦𝘳𝘺 month and bust their budget.

They feel like it’s impossible and useless to keep a monthly budget for this reason.

A budget actually helps you prepare for these expenses using a handy tool called sinking funds!

➡️ Swipe to see how they work!!

Anybody else a budget and spreadsheet nerd ??! 🙋♀️ I could spend hours looking over the monthly budget 😜 #monthlybudget #budgeting #budgetplanner #budgetnerd #marriedfinances #personalfinanceforwomen #budgetspreadsheet

Many people falsely equate being frugal with being broke.

Our culture loves to make you think that the appearance of wealth = wealth.

A while back, I read a book called The Millionaire Next Door, and from this book I learned that the average millionaire:

• Drives a car that is 3-5 years old

• Has never paid more than $50 for a pair of jeans

• Lives in a home less than 3,000 sq ft

• Owns a primary residence worth $300k

What does this tell us? Your neighbor driving a Benz that just put in a pool and remodeled their entire house probably didn’t make the cut 🤷♀️

Either way, you don’t know if they are responsible with money or not, and the data shows us that those who don’t look wealthy are often the ones who are.

Our culture has it 𝘣𝘢𝘤𝘬𝘸𝘢𝘳𝘥𝘴- consume, consume, consume. You 𝘥𝘦𝘴𝘦𝘳𝘷𝘦, you 𝘯𝘦𝘦𝘥, you 𝘴𝘩𝘰𝘶𝘭𝘥 have ______.

Wisdom tells us that the only things we NEED are the essentials, what we DESERVE is not as important as what we can GIVE, and we are not 𝘦𝘯𝘵𝘪𝘵𝘭𝘦𝘥 to anything we can’t pay cash for.

Read between the lies.

There are wise poor and wise rich—and foolish poor and foolish rich. Choose carefully who you learn your habits from ⭐️