Money Saving Tips for People Who Suck With Money

melaniedj • 26 January 2019

I get it. You don’t like budgeting, you hate numbers, and the thought of creating a financial plan makes you want to vomit.

Ok, that might be a tad dramatic, but you get the point.

This comes at a direct antithesis to the fact that you actually do want to manage your money better.

Maybe you’re a natural spender and no matter what you try you can never get your spending under control. Or, maybe you’ve tried budgeting and have a hard time sticking with it. Maybe you’re piled under a mound of debt.

Whatever the case is, you CAN change your habits.

This is near and dear to my heart because my husband is this way. He hates budgeting, financial planning is like a swear word to him.

While we have the same end goals, we have completely different personalities. When you’re dating opposites attract. When you’re married, they don’t.

Needless to say, we had to figure out a way to “trick” my husband into developing better money habits.

Let me point out- there is absolutely NOTHING wrong with the fact that you don’t speak the financial language or care to. That is your personality!

However, if you want to reach your financial goals, just like with any other goal worth reaching, you have to do some things that you don’t necessarily want to do.

Don’t worry, there are some really practical ways you can trick yourself into handling your finances better that don’t require you to keep a 50 page written budget. Even I wouldn’t go for that.

MONEY SAVING TIPS FOR THE NOT SO FINANCIALLY SAVY

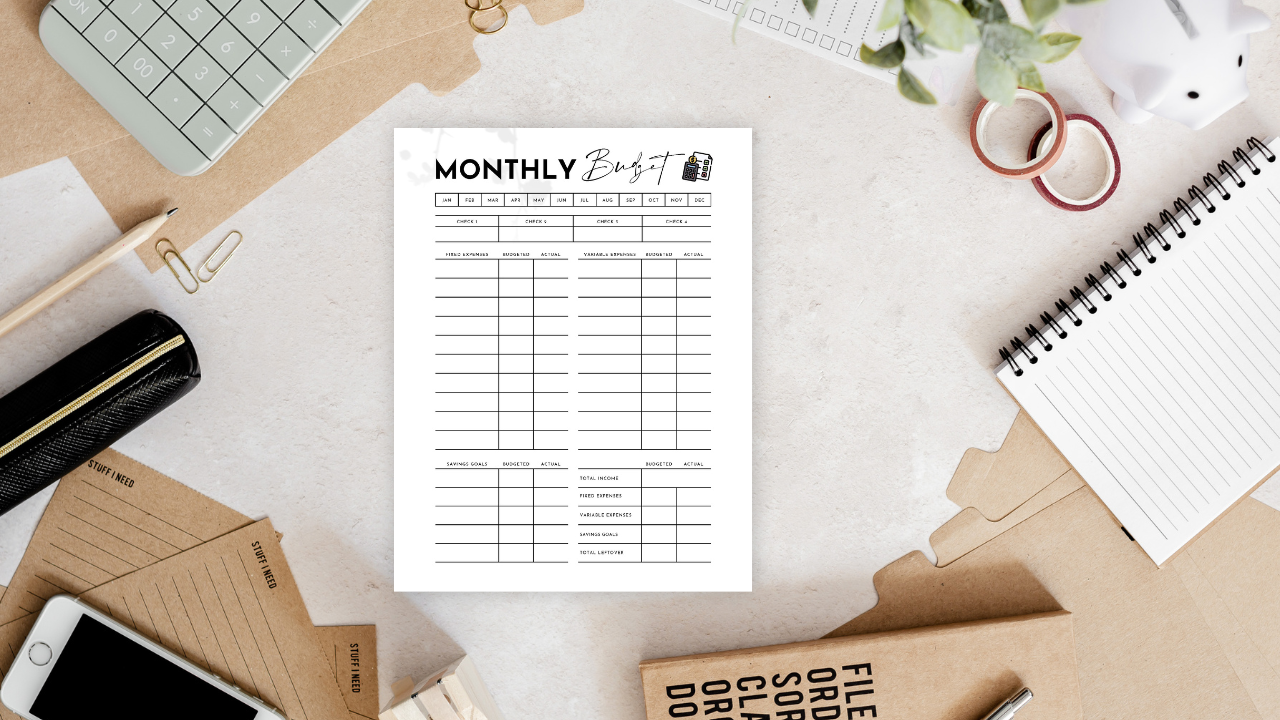

USE TEMPLATES & SPREADSHEETS

If you already hate dealing with your personal finances, you need to make it as easy on yourself as possible. Instead of spending hours creating a budget spreadsheet, use one of the four different styles of monthly budget templates from my budget bundle.

These templates are designed for those who feel like they are always running out of time (and thus their own finances are the first thing to go), for the beginner budgeter, and for those who just don’t like to make their own!

I’ve learned to measure the value of things in units of TIME and dollars. Before, I would only measure in dollars. After having my first child, I’ve realized that my time is absolutely priceless.

There’s a pretty hefty price tag I’ll pay if it means I don’t have to spend my own time doing something.

This is exactly what I believe about the budget bundle and personal financial planning guide. It includes 45+ pages of financial resources to help you take control of your finances.

This bundle will give you everything you need to tackle your finances (even if you hate numbers)!

PAY WITH CASH

Cash is the new credit.

Ok, that might be true only a small, small amount of people. However, that small group is a lot better off because they are not reliant on credit to survive financially.

I loathe credit cards. I don’t care if you pay it off. You’re developing poor money habits. It has been proven over and over that you spend nearly DOUBLE with a credit card as opposed to paying with cash.

This is for two reasons, a concept called coupling and reduced sensation of loss.

First, when there is a time lapse between the purchase of an item and when you have to pay for it, the cost becomes less important. The cost especially becomes less important when it is coupled with other transactions on a monthly statement.

That $50 top doesn’t seem like such a big deal on a credit card statement that totals $300.

Second, when you don’t have to physically hand over money, your brain literally psychologically does not process as much “loss” or “pain” that cash would.

It’s a lot harder to justify a purchase when you’re handing over Uncle Ben to the cashier as opposed to swiping a plastic card.

Please, understand, no matter what argument or justification you give yourself about the rewards, air miles, building up of credit, it has once again been proven OVER and OVER that EVEN with all the rewards, you STILL spend more than you would have with cash!

Credit card companies aren’t dummies. No matter how clever you think you are, you cannot outsmart them!

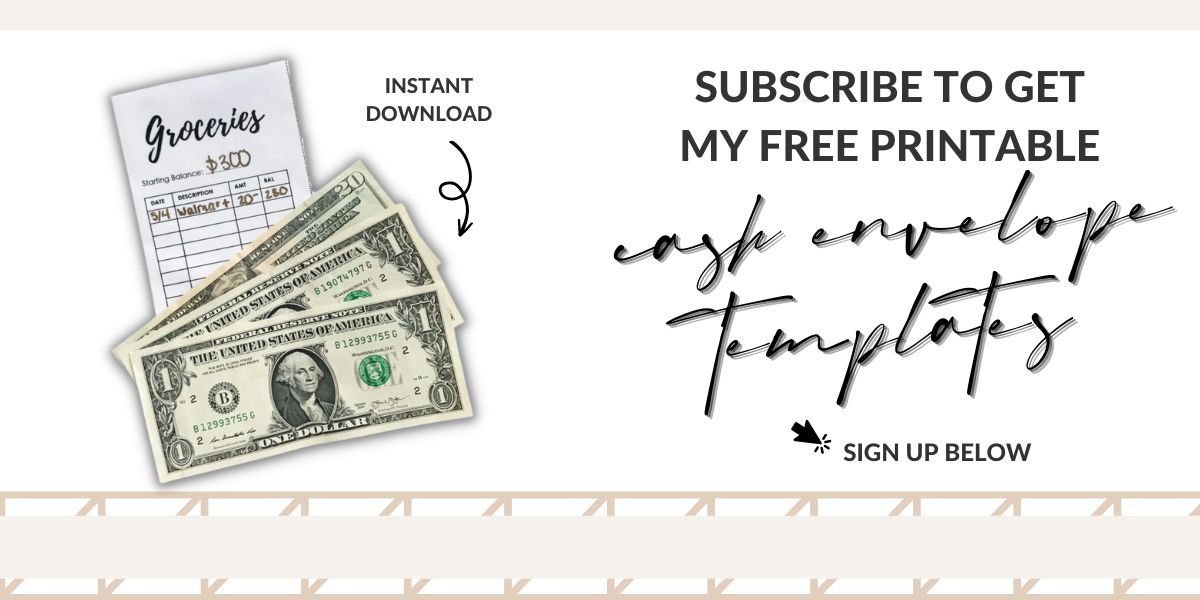

CASH ENVELOPES: THE SECRET TRICK TO CUT OVERSPENDING

I've used these cash envelopes for YEARS to help keep my spending in check.

When you use cash, you feel the weight of your purchases and you're more likely to make smart money decisions.

Whatever budget categories you tend to overspend on, use cash!

The following are great budget categories to make cash envelopes for:

- Miscellaneous

- Gifts

- Groceries

- Personal Spending

- Restaurants/Dining Out

If you sign up for my email list , you can get a set of free plain white cash envelopes that includes blank envelopes (for you to customize) and pre-made envelopes with cute hand lettering font!

TRANSLATE YOUR SPENDING TO HOURS WORKED

For every purchase, compute the number of hours you had to work in order to buy the item.

Let's say you are thinking about going out to a fancy dinner even though you’ve already dined out a few times in a week.

To combat your emotional desire to spent, ask yourself “how many hours did I have to work to make $75?”

If the answer is more than one, just think about the fact that you probably won’t even be at the restaurant more than an hour, and when it’s all said and done you won’t have anything physical to show for it…. Besides maybe a little extra for your spouse to love!

In all seriousness, when you begin to think about purchases in the context of hours worked, you begin to make more conscious spending choices.

AVOID EMOTIONAL SPENDING

You can’t predict your future emotions when you’re creating your budget.

I am not a spender, but when I do spend more than I should have, it’s because I let my emotions get the best of me.

If I’m being honest, I am an extremely emotional person. I would prefer to use the word passionate, because that makes me not sound like such a wreck. But, this blog is for transparency :)

The first step to avoiding emotional spending is to identify what emotions cause you to spend.

Do you overspend when you feel down? Stressed? Angry? Proud?

Once you can identify what emotions cause you to overspend, when you are tempted, implement the 24 hour rule, meaning wait 24 hours before purchasing the item you want.

More times than not, you will be able to calm down and realize you don’t need a THING to fill emotional voids.

Another way that I personally combat this is I make it hard for myself to make purchases.

I do a lot of my shopping online, so I don’t allow any of my debit card information to be saved on websites.

This way, when I do feel like making an emotional purchase, it’s inconvenient to do so.

I have to get up, get my card, re-enter all the information, fill out the billing section, etc.

I know, first world problems.

Do whatever you need to in order to make it inconvenient for you to make emotional purchases.

LISTEN TO PODCASTS

Listen to podcasts that educate, motivate, and encourage you.

If you're not a millennial and you're reading this, I would encourage you to give podcasts a try! If you have a smartphone, you can download Spotify for free and instantly start listening.

They are convenient, informative, and educational.

There are some FANTASTIC podcasts out here to help with money. It’s kind of astonishing that they are free.

Nearly everyone has a library, Google search bar, or podcasts available for use, and thus there is absolutely no excuse for not furthering your knowledge, in this case surrounding the topic of personal finance.

Some of my favorite Podcasts include…

- The Dave Ramsey Show

- Rich Dad Radio Show

- Radical Personal Finance

- Entreleadership

- Catalyst Leadership

TAKE A COURSE

Purchase an online course or interactive book course.

I highly recommend Dave Ramsey’s Financial Peace University. This is without a doubt my number one recommendation for those looking to get on track financially!

This course changed our lives!

I honestly mean that.

If you are looking for something a little more basic to start out with, I have a budgeting for beginners email course that teaches the basics of budgeting as well as beating budget blunders and different ways to track your budget.

The email course is excellent for those who don’t yet have a budget but would like to set one up and need some additional guidance!

AUTOMATE YOUR SAVING & INVESTING

Set up automatic transfers from your bank accounts to your investment and savings accounts.

You gotta do what you gotta do, and when your financial future is at stake, you better get it DONE.

Automating your saving and investing is a good idea even if you’re good with money!

Personally, we automate our saving and investing. Whenever we get paid, I manually transfer the money we have designated for saving to our savings account RIGHT AWAY (this is key).

I like to keep our checking account balance with only enough to cover our budget for the month; the rest goes straight to our savings.

Additionally, at the end of every month, a fixed amount is transferred from our bank account to our mutual fund accounts.

This way, even if I’m tempted to spend money that we have set aside for saving or investing, I can’t unless I go through some big hoops to stop the automatic transfer.

If even the automatic transfer can’t stop you from spending, I bet the overdraft fees will!

More investing tips & advice:

- What You Need to Know About Retirement Planning

- The 7 Most Importan t Money Habits You MUST Know

- 10 Habits to Start in Your 20's to Retire a Millionaire

- How to Invest When it Feels Like You Have No Money

- 7 Things Millionaires Do Differently With Their Money

- The Best Investing Tips Millennials Need to Know

- 7 Surprising I Wish I Knew Earlier About Money

THINK ON IT

Just walk away. Most of the time you won’t come back.

If you are tempted to purchase something that is not in the budget, implement the 24-hour rule mentioned earlier.

I get it, sometimes there is something that you REALLY, REALLY want, and it’s darn near impossible to tell yourself no. You have thought about it day and night. It’s staring you in the face. You’re thinking about all the future memories you’ll have with this item.

I have these temptations all the time! They really seem to surface whenever I enter a Hobby Lobby store.

In these times, allow yourself 24 hours to think/sleep on it.

More times than not, you’ll find that you really don’t NEED the item as bad as you thought.

My husband and I joke when we take shopping trips together, we end up going to five to six different stores, thinking about purchasing a few different items, and then come home empty handed almost EVERY SINGLE TIME.

How do we do this? We don’t make impulsive purchases.

If there is a big ticket item at one store that we want, we almost always agree to “think about it” while we are at the next store.

It never fails while at the next store, we come to realize we don’t really “need” the item, our “want” was just getting the best of us in the moment!

HOW TO IMPLEMENT THESE MONEY SAVING TIPS

My advice would be to implement these one by one.

Research has shown that when you focus on one thing at a time, you are more effective.

Every week, implement one of the ideas/tips above into your life, and watch yourself grow into a natural money-saver!

At the least, you will hopefully be able to develop some restraint and think "bigger picture" about your finances!

Share this post!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

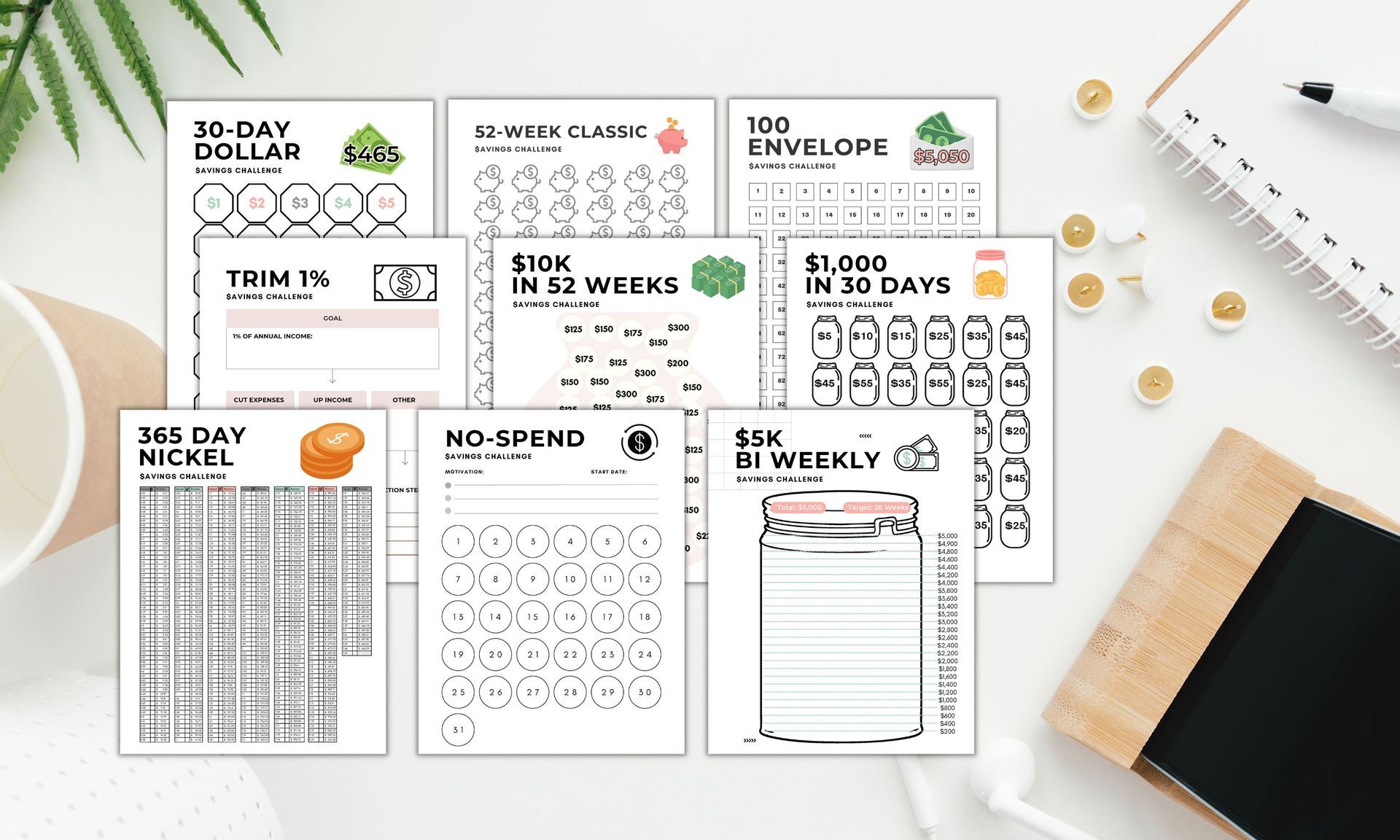

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!