7 Ways to Reduce Financial Stress and Overwhelm This Year

melaniedj • 2 January 2019

Does anyone else see all the New Years posts and think to themselves, I’ve already been stressed, frustrated, and anxious about the new year, and it’s only day one?

I hope I’m not alone!

That being said, some of you are feeling financial stress as we head into the new year. I want to share with you 7 resolutions to reduce financial stress and overwhelm!

A quote that I heard this year in the midst of a busy season really resonated with me. It went like this:

“The difference between the values you embrace the life you live = your frustration.”

If you value financial freedom, but you are in debt up to your eyeballs, you will be frustrated.

When your inability to control your spending means you have no savings for emergencies and thus you’re one financial crisis away from disaster, you will be frustrated.

If your personality craves organization and structure but you do not follow a financial plan or budget, you will be frustrated.

I'm going to help you reduce your financial stress and overwhelm with the following seven resolutions that actually WORK!

HOW TO REDUCE FINANCIAL STRESS AND OVERWHELM

SAVE UP FOR EMERGENCIES

If you are really serious about taking control of your finances this year, you need to save up money for emergencies.

There’s a favorite story I like to tell myself at the start of every year. It goes like this….

Unlike this past year, we won’t have any major, unexpected expenses. This year will be the BEST yet. All will go as planned. Joe’s truck won’t need a $5,000 repair again, we won’t have any major home repairs because we just replaced the dishwasher, and we for sure won’t have to almost sell our child to pay his hospital bill!

Spoiler alert… WRONG

.

Unexpected things WILL come again. The year will not go as perfectly planned by the queen of financial planning, much to my dismay.

BUT, that does not mean we throw in the towel and say screw it.

Every single major unexpected financial expense has been way less stressful than it COULD have been. Why is that?

It’s because we budget, and we save for emergencies.

A good goal is to have 3-6 months of household expenses (the necessities) in your savings. Then, DO NOT touch this savings unless there is a legit emergency.

Hint: A new dress for a wedding is not an emergency. Replacing your couch is not an emergency. Those concert tickets are definitely not an emergency.

An emergency fund gives you a financial cushion as well as financial peace.

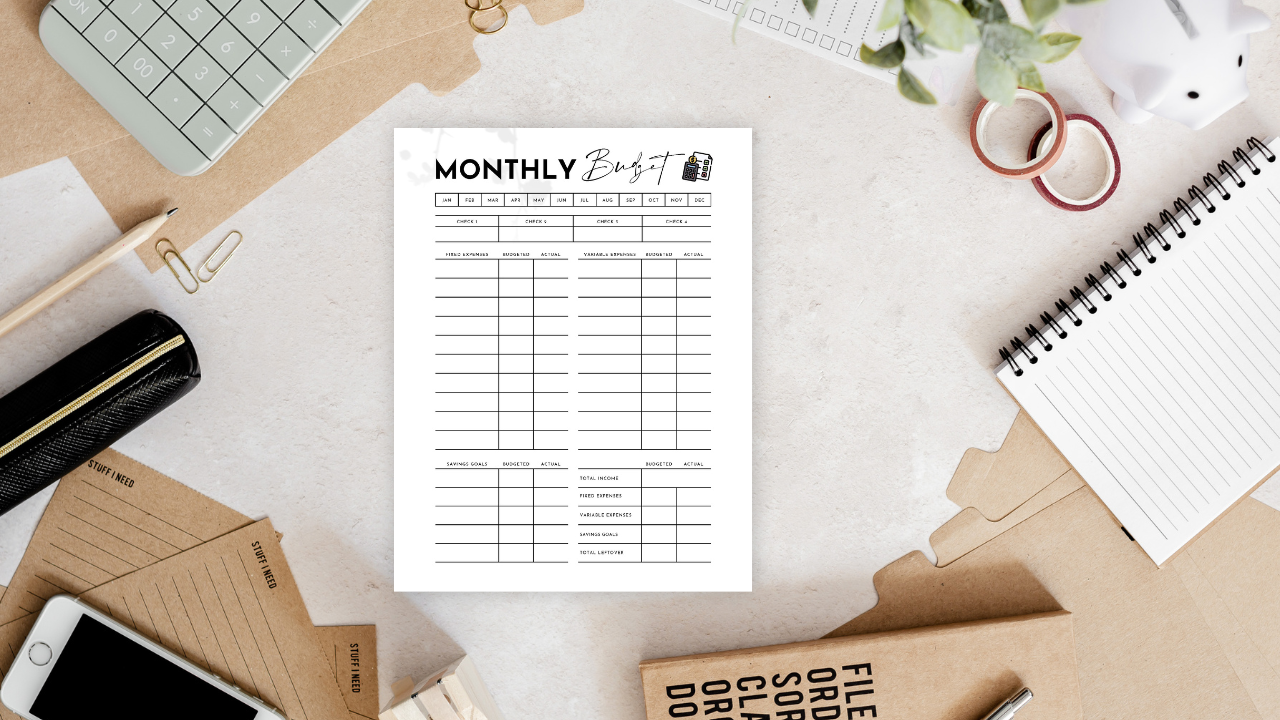

USE A BUDGET

Create and follow a monthly budget and focus on what you CAN control.

You CAN control how you plan to spend your money. I’m not saying that things are always going to go according to the budget.

The car will break down. You’ll have an extra impromptu dinner with friends that wasn’t in the budget.

However, having a budget that you stick to (for the most part) not only gives you peace of mind, but it helps you prepare for financial surprises that cause stress.

Instead of being stressed and crabby when the car breaks down and costs $800 to fix, if you budget and set aside money every month in a car repair fund, you don’t have to let the car repair cause financial stress, because you already have the money!

A budget drastically transformed our finances. When we started to use a budget, it suddenly felt like we had more money every month!

Once you start budgeting, you'll be surprised at how much money you THOUGHT you were spending and how much money you are ACTUALLY spending.

Trust me, they are usually two very different amounts!

If you are experienced at budgeting, download my free monthly budget template by subscribing below!

I lay out exactly how to set up your budget as well as give you tips for maintaining your budget!

BREAK UP WITH YOUR DEBT

You need to kiss this unhealthy relationship goodbye this year.

It’s hard to build any kind of wealth or savings when your income is tied up in monthly payments. If you are in debt, you have fallen prey to the idea that affordability is determined by a monthly payment,

not the total price.

Broke people ask how much down and how much per month?

Wealthy people ask how much?

If you are in debt, no matter what kind (car, student loan, personal loan, home equity loan, etc.), there will come a day when it will become overwhelming.

Bills tend to increase year to year, and with a monthly payment that doesn’t go down, debt becomes a key stressor.

DEVOTE 20 MINUTES A DAY TO SELF-EDUCATION

Self-education is vital to success.

Take your education into your OWN hands, don’t leave the job to a school.

I learned a lot more from books I’ve read on my own than sitting behind a desk for six hours everyday.

I don’t care if you have a masters degree, a bachelor's degree, or no formal education. You have the tools available to you to learn whatever it is you want.

That’s how some of you ended up on this blog, you want to know more about paying off debt, budgeting, frugal living, or saving money.

If you want to handle your finances better this year, start listening to podcasts, reading books, reading my blog (had to throw that in there), or watching youtube videos.

I know that life is busy, so set a goal to invest 20 minutes a day into learning more about something.

Cut out that hour you spend on your phone scrolling through social media after work and do it then!

SET BIG GOALS AND SMALL SUB-GOALS

The best way to ensure that you meet your BIG goals, is to set SMALL goals.

The best way to do this is to set both short-term and long-term goals, and then to write them down often and put them somewhere that you can see them everyday.

Here are some great ideas for goals to set in the new year!

SHORT-TERM GOALS TO SET

- Develop & stick to a budget

- Pay off all debt (besides your mortgage)

- Establish and fully-fund an emergency fund

- Invest (at least) 15% of your gross income

- Save for a ___________________

LONG-TERM GOALS TO SET

- Pay off home early

- Fund kids college

- Retire at age _____

These are just some examples, but seriously think about where you want to be financially in five, fifteen

, and thirty

years from now.

Do you want to be stressed when you’re only fifteen years away from retirement because you’ve put off investing? Would it feel good to have your home paid off early? What do your kids college funds look like?

These are all things you need to think about NOW.

Don’t wait, friend!

Think about and set these financial goals (with your spouse if you’re married), and then write them down. ALL THE TIME. Take them out and read them.

Remind yourself often of where you want to go!

AUTOMATE YOUR FINANCES

The percentage of your income that you save and invest is more important than the size of your paycheck.

You don’t have to make a fortune to be a millionaire when you retire, you just have to be disciplined.

In order to save and invest, you have to practice self-discipline. No one else is going to make sure that you are able to retire with dignity. It’s not anyone else’s job!

If you have trouble being disciplined, automate your saving and investing.

Just like bills come out of your account automatically every month, set it up so that your retirement contributions or transfers to your savings account are automatic.

Do what you have to in order to make sure that you are saving and investing.

FIND SIMPLE WAYS TO SAVE MONEY (DON’T OVERTHINK IT)

When many people think of saving money, they think of time-consuming, difficult things that just add more stress and do more harm than good.

Yes, there are some articles you’ll come across that suggest ways to save money that are rather time-consuming and just not worth it!

I understand the time overwhelm.

If there is one thing I’ve learned this year it is that time is my most valuable, non-replenishable

resource.

I am super frugal and I love to save money. However, the things I do to save money have to create more time for me AND save me money.

Here are a few things that I did this year to save money

AND time.

#1) I Invested in a Meal Planning Service

I was apprehensive at first about trying any sort of service. In my mind, I could do anything cheaper myself.

Boy was I wrong (and I'm glad I was)!

I invested in $5 Meal Plan and I honestly could not be happier that I did! This meal planning service saves my butt every single week.

As a mom, wife, full-time CPA, and blogger, I barely have time to take a shower longer than three minutes let alone plan my meals AND grocery list for the week.

With $5 Meal Plan , I pay $5 a month to have my meal plan for the week sent to me every Friday, and it includes an organized grocery list.

HELL. YEAH. Total mom win.

Also with my subscription, I have access to an entire recipe bank where I can sort and filter by what kind of recipe I want. I use this if there is a meal on the meal plan that I know my husband won't like!

#2) Use More Freezer Meals for Busy Seasons

Most of the time, you know when a busy season in life is about to begin. That season for our family is when I'm in tax season.

Since I know this, I prepare. My meal planning service is not enough during this time because during tax season it's a miracle if my hair gets brushed in the morning.

You think I'm kidding.... I'm not.

Thus, I have another handy-dandy frugal tip, I use freezer meals!

This way, I am not tempted to eat out and my husband is not as tempted to eat out either because if I'm not home, he can quick grab a meal from the freezer!

If you don't have time to prep freezer meals, the same meal planning service I used also has a freezer meal service!

Through the month of January, they are offering a free freezer meal challenge!

The challenge officially starts January 2, but you can sign up now!

Now is a good time to check it out!

You can also check out their freezer meal starter kit and customized freezer meal products , designed so you can prep 8-10 meals in 1 hour!

#3) Cut Cable

We (moms specifically) are always complaining about how we don't have any time.

It's true, we are busy, but I bet if you checked how much screen time we have in a day between the TV and our phones you'd tell us that we can FIND and MAKE time if we would cut out our screen time!

Keep it simple- cut the cable cord!

This will save you time AND money!

MAKE IT A GREAT YEAR!

Finally, I want to leave you with some encouragement.

No matter were you found yourself at the end of this past year, you have the power to make this the best year yet.

You have the power to make the year after this the best year yet... and the next.. and so on so forth.

Changing where you are is as simple as making a choice, and then changing your thoughts and taking aggressive action.

Your thoughts are just as important as the actions you take. Our thoughts are SO powerful.

Start imagining where you want to be a week from now, a month from now, a year from now.

Write down your financial (and other) goals as if you have ALREADY accomplished them.

Take massive action.

Enjoy the process.

Share this post!

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!

Step by step guide to creating a zero based budget worksheet that will help you track your income, fixed and variable expenses, savings goals, and debt tracking on a monthly basis.

Where do high-yield savings accounts fit into the financial plan for the productive Christian household? Are these types of savings accounts a wise investment for leaving an inheritance for our children’s children and stewarding the resources allotted to us? What are the potential risks associated with these accounts, if any? How can these accounts be utilized to meet your family finance goals? Are they only for the wealthy with tons of excess cash?

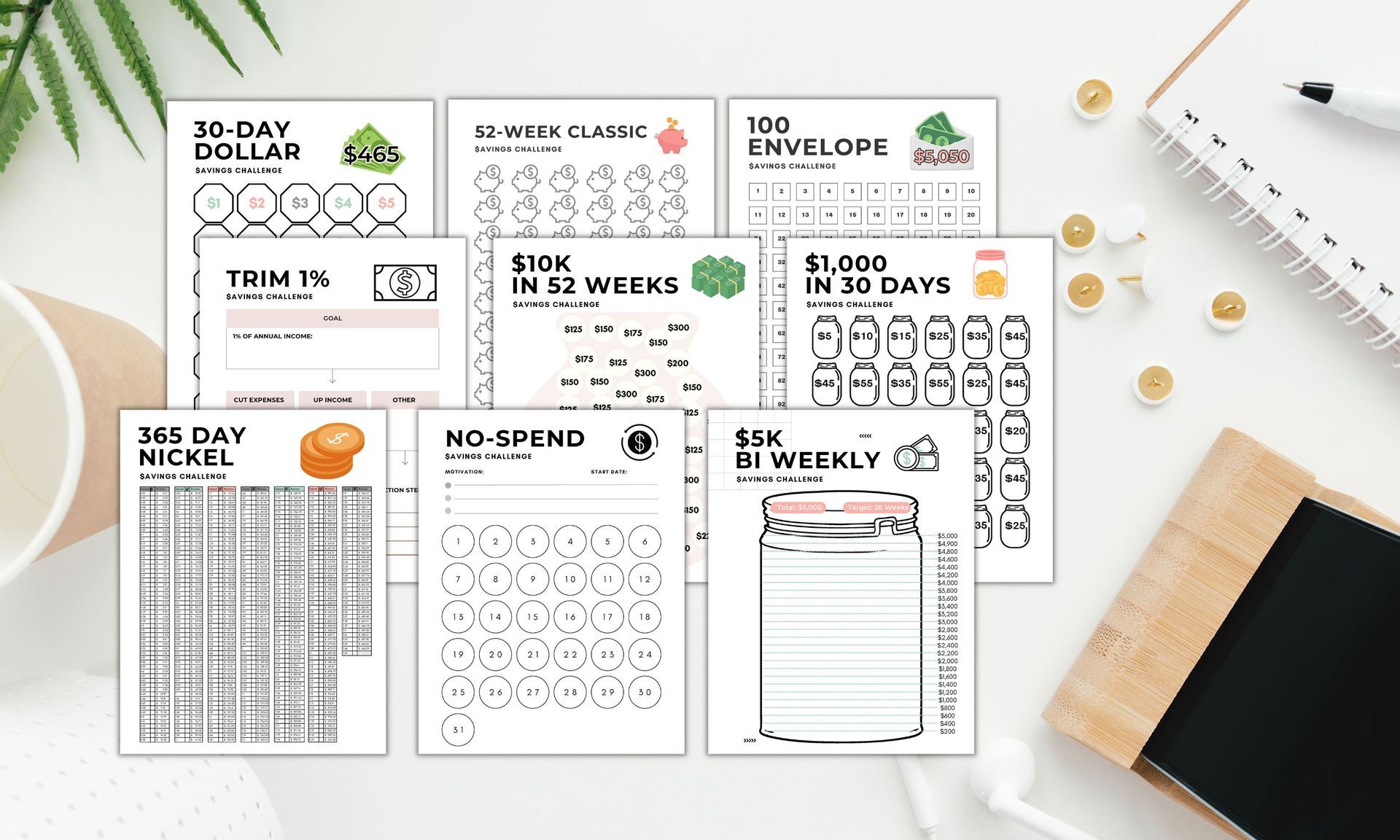

One of the best money saving strategies is to complete a savings challenge. Try the penny challenge, envelope challenge, 10k savings challenge, or any of the other money challenges outlined in this post to save money quickly!

Step by step tutorial how to make a budget in excel or google sheets. Plus, get my free google sheets budget template that can be exported to excel in just a few clicks! Creating an excel budget will save you time and make budgeting a seamless process.